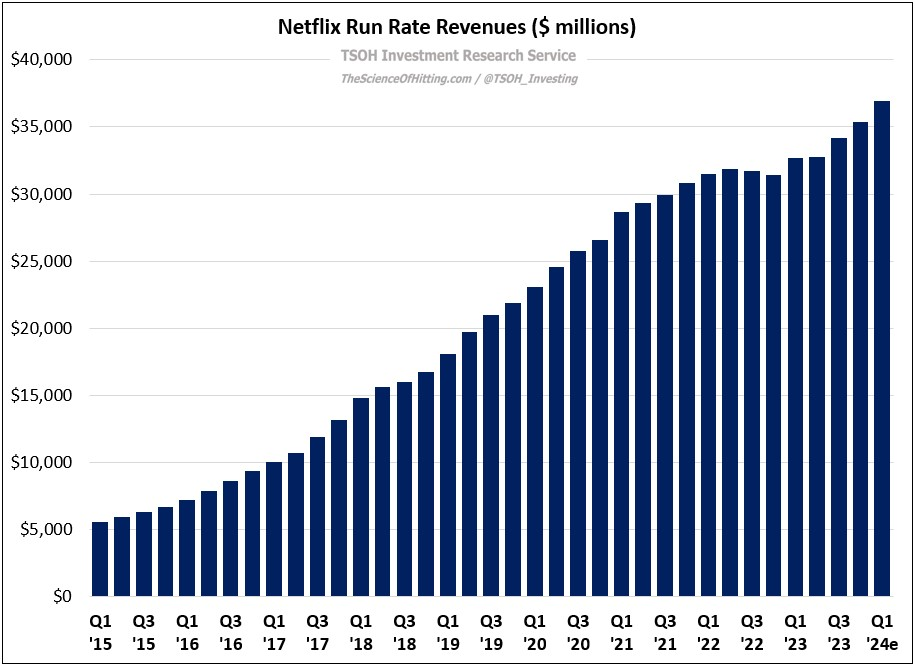

Netflix: Reaping The Rewards

The past few years have been a wild ride for Netflix.

The most notable tough stretch of late came in early 2022, when subscriber growth and profit margins both came under pressure (and at a time when competitors were investing aggressively to scale their DTC services). As I noted in April 2022, I believed that what was perceived as a Netflix-specific issue was more likely a canary in the coal mine for broader media industry pressures - and it would soon lead to difficult decisions for legacy competitors who were relatively new entrants in DTC VOD / streaming. As we approach the two year anniversary of the April 2022 write-up, it’s interesting to consider the choices and outcomes we’ve seen subsequently. First, the next round of media industry M&A has proved elusive; whether that represents an inability or an unwillingness (a clear logic) for the next big deal is an open question. Second, while Netflix continues to make incremental investments to support the next leg of global growth for its business (from volumes and pricing), competitors have begun to reduce their (net) DTC content spend, along with other key operating expense lines like marketing. Third, streamers continue to evolve their DTC content offerings, with the most notable example being their most popular sports rights – putting further pressure on the U.S. linear TV business (which, as a reminder, typically covers their large DTC losses).

Amidst continued change in the media industry, and with the possibility of unexpected and substantial developments on the horizon (M&A), one thing I personally remain confident in is the sustainable competitive advantages that Netflix has established in DTC VOD / streaming. This is a company that has long recognized where the puck was going and accepted the significant costs required to achieve long-term success. They are reaping the rewards for decisions they made 10 months ago, as well as 10 years ago. With that said, the sustainability of their advantages isn’t God-given; it demands a continued commitment to their strategic vision, along with a willingness to reconsider new opportunities as their business and the industry continues to evolve. As I’ll discuss today, I believe Netflix’s results over the past 24 months, along with this week’s WWE deal, are indicative of a company and a management team that recognizes the huge opportunities that remain on the horizon.

UCAN

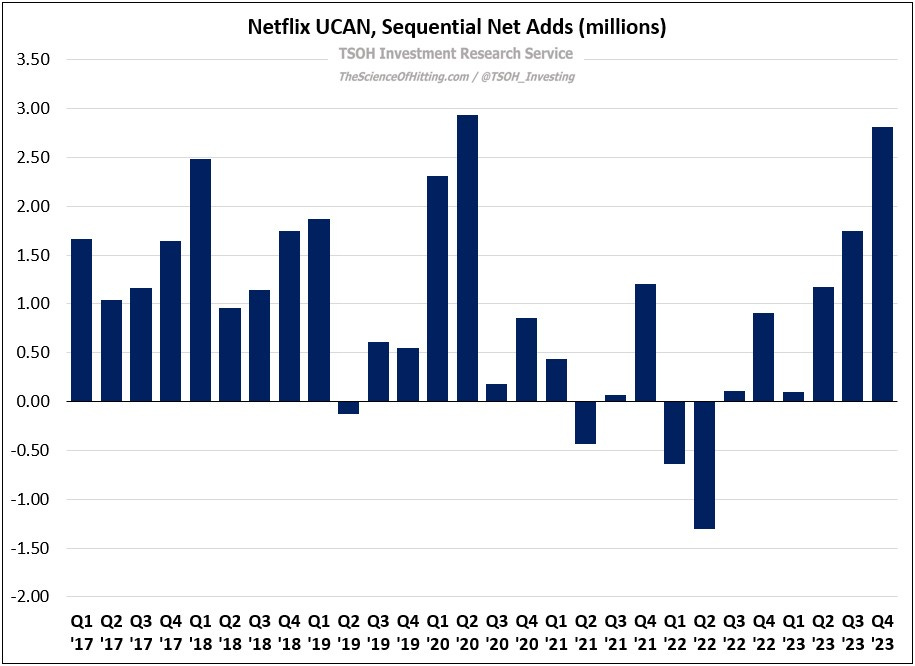

Let’s start with an update on the Netflix UCAN growth algorithm. As I noted in October, Netflix added 1.8 million net paid subs in the region in Q3 FY23, its highest sequential gain in 18 quarters (excluding the pandemic tailwind quarters in Q1 FY20 and Q2 FY20). The Q4 FY23 results were even more impressive, with Netflix adding 2.8 million incremental net paid subs – the largest sequential UCAN increase since Netflix began breaking out regional figures in 2016 (again, excluding Q1 FY20 and Q2 FY20). Here’s another way to think about this change in UCAN volumes: one prominent industry analyst came into 2023 estimating that Netflix would reach ~78.5 million subs in the region by yearend 2026. The fact that they’ve already eclipsed 80 million subs is further evidence that the playbook is working.

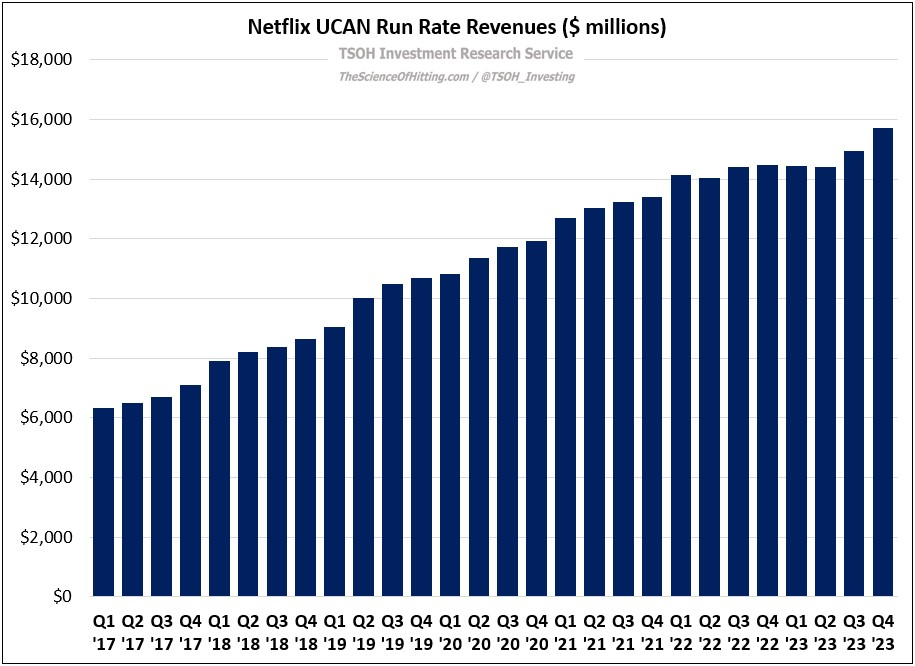

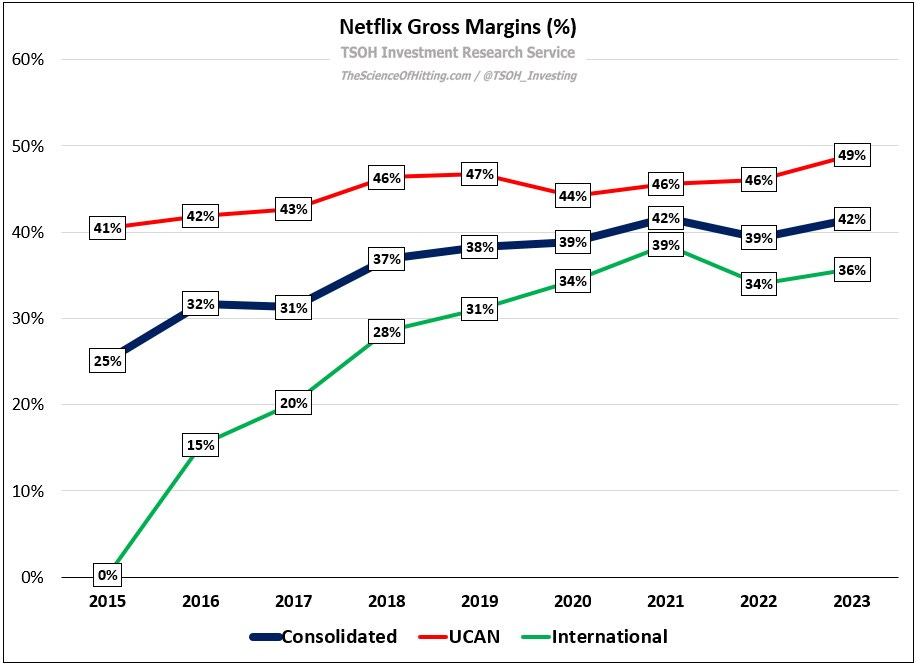

In terms of the financial implications, Netflix UCAN now generates ~$16 billion in run rate revenues (+9% YoY). While the growth algorithm was weighted towards volumes in 2023, I think pricing / rate will take the reins over the next 12-24 months. That outcome is supported by the ongoing content and platform investments Netflix has made over the past 15+ years, as well as opportunism that has led to licensing desirable content from legacy media companies who have quickly concluded that they need to rethink their DTC VOD strategy (even in the U.S., which is presumably their strongest market). In addition, as you can see in the second chart below (updated from “Regional Economics and Global Scale”), I estimate Netflix’s UCAN gross margins reached record levels in 2023. As others make drastic changes in search of an answer to sustainable long-term economics in streaming, Netflix is playing offense in UCAN while also reporting impressive financial results.

International