Netflix: Regional Economics and Global Scale

In a recent Chit Chat Money podcast, I said the following about Netflix:

“I think it’s really important to try to look at this company regionally, to get a feel for how these different businesses are tracking. If you look at a region like the United States [UCAN], obviously the product and the subscriber base is much more established than in other markets around the world… It’s a mistake to view Netflix as a single business. You need to think about where these different regions are at in terms of their lifecycle.”

To date, I have not sufficiently explained why I think this matters.

Today’s write-up is my attempt at rectifying that for subscribers.

In the Q3 FY19 letter, Netflix management disclosed that they would alter their segment reporting: “Starting with our Q4 2019 earnings report in January 2020, we plan to disclose revenue and membership by region, which is how we think about our business. Our four regions are Asia Pacific (APAC), Europe, Middle East & Africa (EMEA), Latin America (LATAM), and the US and Canada (UCAN). UCAN is roughly 90% US and 10% Canada.”

As a result of this reporting change, we no longer had access to regional income statements (it’s presented as a consolidated / global P&L). But notably, in the years preceding this shift (2019 and earlier), the company provided a basic income statement for the Domestic Streaming segment and the International Streaming segment. While it requires some assumptions in the out years, as well as some adjustments to align the historic data with the current (four region) reporting convention, we can use this data to draw some important insights into the evolution of Netflix’s regional financial results over the past seven years. For example, here’s a COGS breakdown (mix) between Domestic Streaming and International Streaming.

As you can see, the COGS mix shifted greatly over this period, reflective of aggressive investments behind its International business as the company pursued global scale (for what it’s worth, the International sub base increased by ~7x over this period, from ~14 million subs to ~99 million subs).

Unfortunately, we don’t have regional COGS data for 2020 or 2021 (under either reporting methodology); for this analysis, I assume the mix continued to shift towards International by 250 basis points per year (from 2016 – 2019, International increased by ~300 basis points per year). The net result is that the 2021e COGS mix is ~65% International and ~35% Domestic.

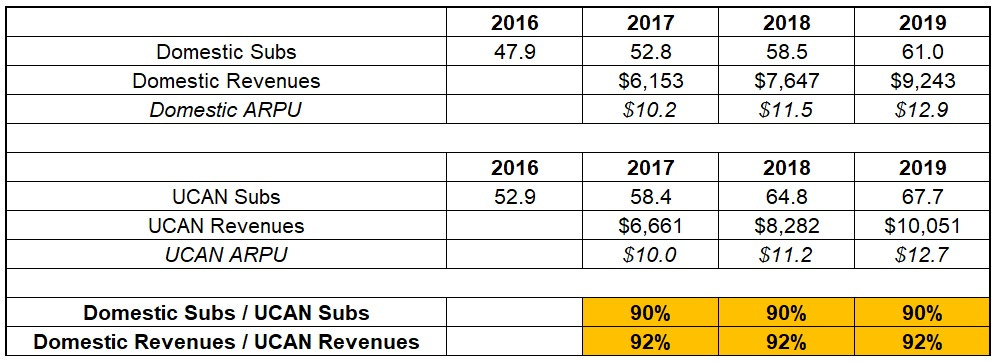

Now we need to look at subscriber / revenue data. Thankfully, the 2019 annual report included some historical figures for UCAN and Domestic.

As you can see, the results from 2017 – 2019 are aligned with the disclosure in the Q3 FY19 letter (~90% U.S. and ~10% Canada). In order to align this analysis with the current reporting convention (UCAN), I will increase the Domestic subscriber base and revenues in the years prior to UCAN data by ~10%. Of course, we also need to make an adjustment on COGS. In addition to the breakdown discussed above, I will increase Domestic COGS ($) by ~10%, with an offsetting reduction in International COGS. With those adjustments, here’s some key regional financial data from 2014 - 2021.