TSOH Weekly Roundup (04/24/26)

TSOH Weekly Roundup #4

Welcome to the fourth edition of the TSOH Weekly Roundup, which will be in your email inbox each Friday at 11am ET. Each update features a Chart of the Week and a brief discussion on three news items relevant to the TSOH investable universe. If you have feedback on this format, please let me know.

Chart Of The Week

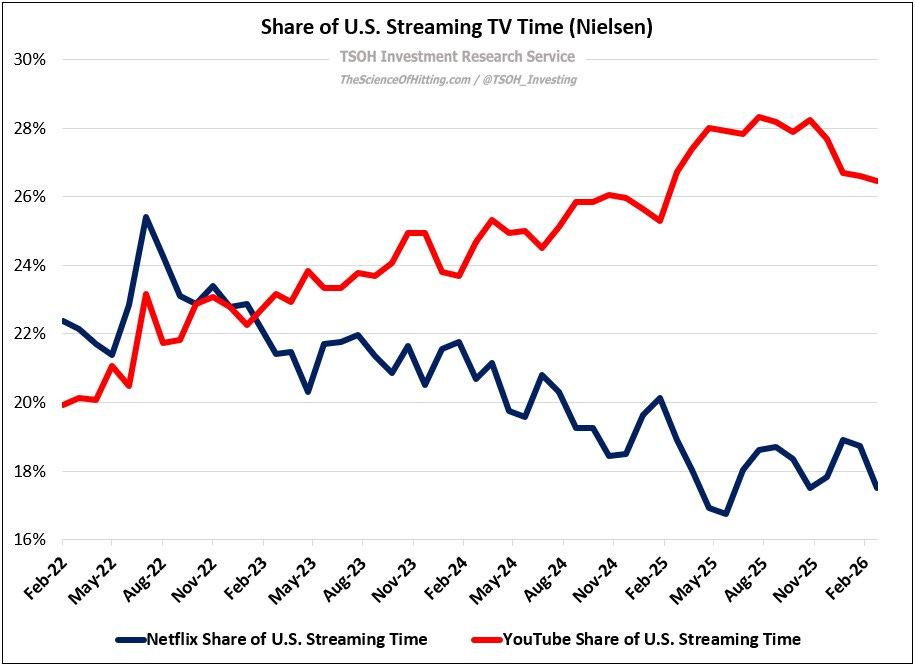

As discussed in Monday’s update, impressive near term financial results have not assuaged Mr. Market’s concerns about Netflix’s exposure to changes in the media / entertainment industry. One data point that encapsulates this concern is Netflix’s declining TV streaming market share (engagement) in the U.S., during a period where YouTube has been trending in the other direction. While there are nuances to appreciate here, this highlights a key concern weighing on the stock, with the EV/EBIT multiple contracting to ~25x forward.

Three Notable Items

“Greg Abel Has Been Leading Berkshire for 100 Days. Things Are Already Changing.”

This WSJ article about Greg Abel’s first 100 days as CEO of Berkshire Hathaway has a few interesting tidbits, including commentary on his working relationship with Ajit Jain, as well as efforts to address the challenges at BNSF and BHE (discussed in my recent Berkshire update, “Transition”).

“Abel has spent the past year giving priority to learning Berkshire’s insurance business and visiting with Ajit Jain, the brains behind the operation. Jain is expected to continue heading insurance at Berkshire, though the company has developed a succession plan for him, too. ‘He’s probably going to be at the company for as long as he can,’ Buffett said in an interview. Berkshire’s new CEO has also emphasized spending time with leaders at subsidiary companies, particularly with BNSF Railway, its railroad business, and Berkshire Hathaway Energy (BHE), where he was CEO for many years.”

“Disney Debuts Giant Screen Brand for Cinemas to Rival Imax”

While I question whether the structure of this collaboration will be effective, this news speaks to the desire of the large movie theater chains to develop alternative PLF solutions (see the historic IMAX / in-house PLF data that I discussed in the IMAX initiation). With that said, consumers continue to vote with their wallets: IMAX reached a record high share of the global box office in 2025, continued evidence the brand / product is seen as being in a class of its own. (As Gelfond argues, “We have nothing in common with the PLFs.”)

“Disney is partnering with movie theater chains on a new large-format screen certification [‘Infinity Vision’] that will roll out in time for ‘Avengers: Doomsday’ in December 2026… Close to 5,500 screens globally - about three times the number of Imax venues - would meet the standards for the new label... The founding of ‘Infinity Vision’ is in part the result of the fact that ‘Doomsday’ doesn’t have exclusive access to Imax’s screens when it opens the weekend of December 18th. Imax has an agreement to screen ‘Dune: Part Three’ the same weekend. Disney contributes more to Imax’s revenue than any other Hollywood distributor… Theater chains began holding conversations last year about establishing an industry-wide certification for their premium screens… Operators would still be able to offer their own big-screen [PLF] brands.”

“Interview: Kinsale Capital CEO, Michael Kehoe”

This was an informative interview with Kinsale founder and CEO Mike Kehoe. As it relates to Kinsale’s long-term competitive position in E&S, this quote from Simon Wilson, CEO of Markel Insurance, has stuck with me: “[Markel] has this fabulous business at the center… and we almost took it for granted that we’ll continue to win… Kinsale went right into wholesale and specialty E&S and started writing at a mid-70’s combined ratio. We took our eye off of the ball in our bread and butter business.” It’s early days, but I assume Wilson is focused on doing what he can to slow / reverse that development.

“If you’re opening a restaurant, your core competency is the cooking, the recipes, and the ambience. What is the core competency of an insurance company? It’s segmenting and pricing risk, it’s underwriting… Why on earth are you outsourcing what you should be striving to improve all the time? It undermines the value of the company… I just wonder why many insurance companies feel like outsourcing their core competency is a great idea.”

TSOH Updates

Here’s the updated TSOH research list for the past six months:

Monday’s research report will be an update on Ally Financial (ALLY).

Have a great weekend!

NOTE - This is not investment advice. Do your own due diligence.

I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information presented in this report. Assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Projections are based on a number of assumptions, and there is no guarantee that they will be achieved. TSOH Investment Research is not acting as your advisor or in any fiduciary capacity.

Great post. I wanted to push back slightly on your argument that Netflix has "declining engagement". I disagree with the framing. You are comparing NFLX share of U.S. streaming time against YouTube’s over the last 4 years, but the more accurate way is to look at NFLX share of TOTAL U.S. TV time.

By using "streaming" as the denominator, the data becomes unintentionally skewed. Streaming is a subset of all TV; while the category is growing as it takes share from broadcast/cable, YouTube has been growing at a faster YoY rate than Netflix. So while YouTube’s share within the streaming category is rising and Netflix’s is shrinking, this ignores the fact that total streaming hours are increasing overall in aggregate.

In my view, the Nielsen Gauge report remains the cleanest measure of total TV viewing market share. From Jan 2025 to Jan 2026, streaming grew from 43% to 47% of total U.S. TV time. Both YouTube and NFLX grew total viewership, the #1 and #2 platforms for total TV time. So the idea Netflix engagement is declining is not true. While others share this perspective, I believe their $25 billion buyback program will eventually prove the point.

Keep up the great work with TSOH; I would simply suggest changing the framing from "Share of Streaming" to "Share of Total TV” and you will see that both Netflix and YouTube can win! Thanks — Accrued Interest (Sim)