Berkshire Hathaway: Transition

January 1st marked the end of an era: for the first time since 1970, Warren Buffett is no longer the CEO of Berkshire Hathaway. His successor, Greg Abel, steps into a situation where some of the most pressing matters for the conglomerate – operational challenges at a few of Berkshire’s largest subsidiaries and the effective allocation of a massive (and growing) cash hoard – have lingered for the past few years. As I’ll discuss today, it’s encouraging to see Greg hit the ground running. I suspect the coming years will reveal why Warren and Charlie concluded he was the man for the job.

Capital Allocation and Alignment

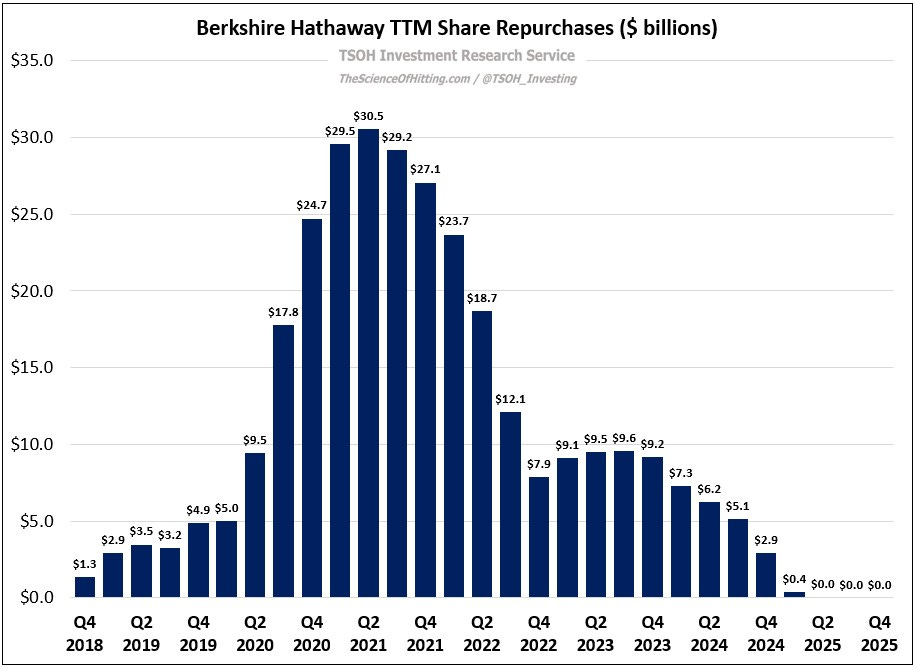

First, following minimal repurchase activity over the past two years – $2.9 billion in 2024 and zilch in 2025 – Berkshire recommenced repurchases in early March. While I expect repurchase activity to remain opportunistic, in terms of the level of aggressiveness at any time, I also suspect we are witnessing the transition to a more persistent level of spend, a pressure release valve on a cash pile that now exceeds $370 billion. Said differently, I think they are becoming less stringent on the price / intrinsic value gap for any repurchases – and I think that’s sensible given the difficulty that they’re having in finding a great use for the next ~$10 billion, let alone ~$100 billion.

Second, Greg recently purchased ~$15.3 million of Berkshire Hathaway Class A common stock, which will be roughly equal to his 2026e after-tax compensation. As he discussed on CNBC, he is committing to annual purchases of Berkshire stock equal to ~100% of his after-tax compensation:

“Absolute alignment with our shareholders is critical; the goal was to continue to demonstrate alignment with owners… I’m committed to doing this every year, as long as I’m CEO… I’ve never been given a share of Berkshire. Our shareholders use their after-tax dollars to buy Berkshire; I’ll do the same.”

As is typical of Berkshire, this is a straightforward way to clearly operate in alignment with long-term owners; it’s not necessary to have byzantine proxy filings with a long list of KPIs that inevitably result in massive equity awards to the C-suite executives. Ideally, more companies and more leaders throughout corporate America would follow the example set by Berkshire and by Greg.

Berkshire Hathaway Energy (BHE)

In June 2022, Berkshire acquired Greg Abel’s remaining ~1% stake in BHE for ~$870 million, or an implied valuation of ~$87 billion. Less than two and a half years later, in late 2024, Berkshire acquired an ~8% stake in BHE held by the descendants of Walter Scott Jr. for ~$4 billion, or an implied valuation of ~$49 billion – down more than 40% compared to mid-2022. (Following the transactions for the remaining ~8%, Berkshire owned 100% of BHE.)