TSOH Weekly Roundup (04/03/26)

TSOH Weekly Roundup #1

Welcome to the first edition of TSOH Weekly Roundup, which will be in your email inbox each Friday at 11am ET. Each update features a Chart of the Week and a brief discussion on three news items relevant to the TSOH investable universe. If you have feedback on this format, please let me know.

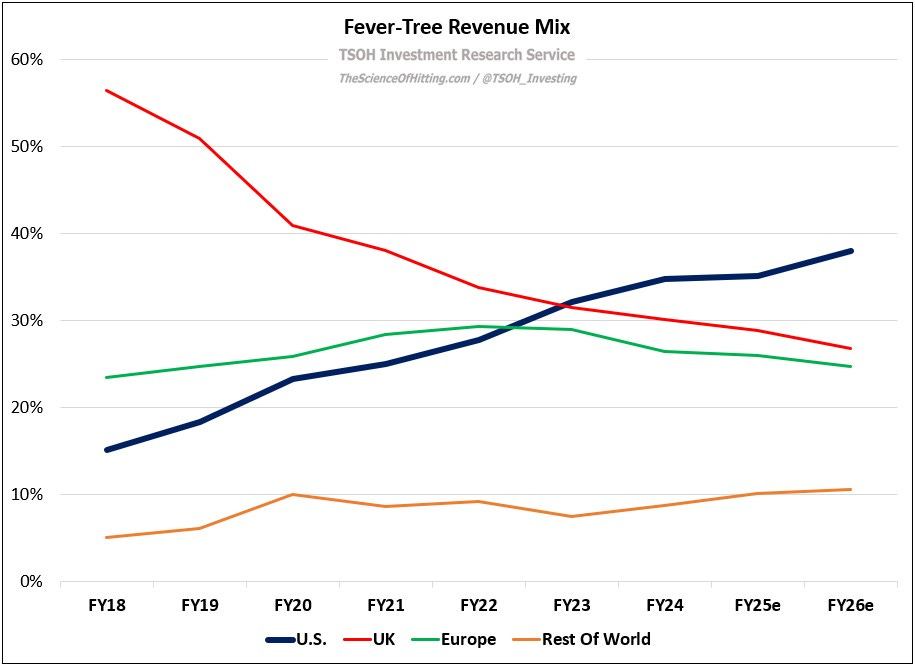

Chart Of The Week

As I discussed on Monday, the transformation of Fever-Tree’s geographic exposure and product mix continued in FY25; it will accelerate further in FY26 as the strategic partnership with Molson Coors transitions to an offensive posture (“roughly doubling” U.S. marketing support). In combination with the meaningful decline in exposure to UK Tonics - now ~20% of Fever-Tree’s business - I believe we’re set to see a meaningful revenue reacceleration.

Three Notable Items

“Pernod Ricard in Talks to Combine With Brown-Forman”

As I’ve noted in my research on Brown-Forman, a key question is whether the interests of the controlling family and minority shareholders are truly aligned. These discussion with Pernod, along with the hasty $400 million share repurchase completed in late 2025, are notable developments.

“Pernod, based in Paris, oversees a portfolio of 200 spirits brands, including Jameson Irish whiskey and Beefeater London gin, and has a market value of around $17 billion. Brown-Forman is best known for its whiskeys; it has a market value of around $12 billion… The deal being considered includes a significant stock component, and the families behind the two companies would likely each retain significant stakes in any deal, they added.”

“Amazon’s Rural Delivery Push Slams Into Walmart”

While this article is focused on competitive dynamics between Amazon and Walmart, it sheds light on the competitive landscape for cost-effective and convenient (timely) order deliveries in rural areas. To me, it helps illuminate the value of Dollar General’s unique store footprint, which enables them to sustainably offer delivery speeds in DG markets others will struggle to match.

“The company’s USPS contract isn’t public, but in 2015 Bernstein analysts estimated that the U.S. postal service was delivering some 40% of Amazon packages for about $2 apiece, about half what UPS and FedEx charged at the time. UPS currently imposes a $16.50 surcharge for residential deliveries in many rural areas… Amazon wanted a cheaper alternative, hence outsourcing rural deliveries to small businesses hungry for a side gig.”

“Reed Hastings: How Netflix missed out on Warner Bros.”

I was somewhat alarmed by the price tag when Netflix inked the Warner Bros. deal, because I believed it transferred too much value to the seller from synergies / improvements that were unique to Netflix’s ability to effectively monetize the assets. That was followed by concerns that Netflix may end up paying 10% - 20% more if (when) dragged into a bidding war. In the end, management made what I believe was the right decision: they told WBD in early December this was their “best and final proposal”, and they meant it.

Hastings: “I generally have not been a fan of M&A… but the particular deal we struck [for Warner Bros.] was at a good price, and I was very excited about getting it done. Paramount decided to pay more, and our co-CEO’s, Ted [Sarandos] and Greg [Peters], decided to not take the bid up any higher… A lot of M&A doesn’t work out, but some work out fantastically.”

TSOH Updates

Here’s the updated TSOH research list for the past six months:

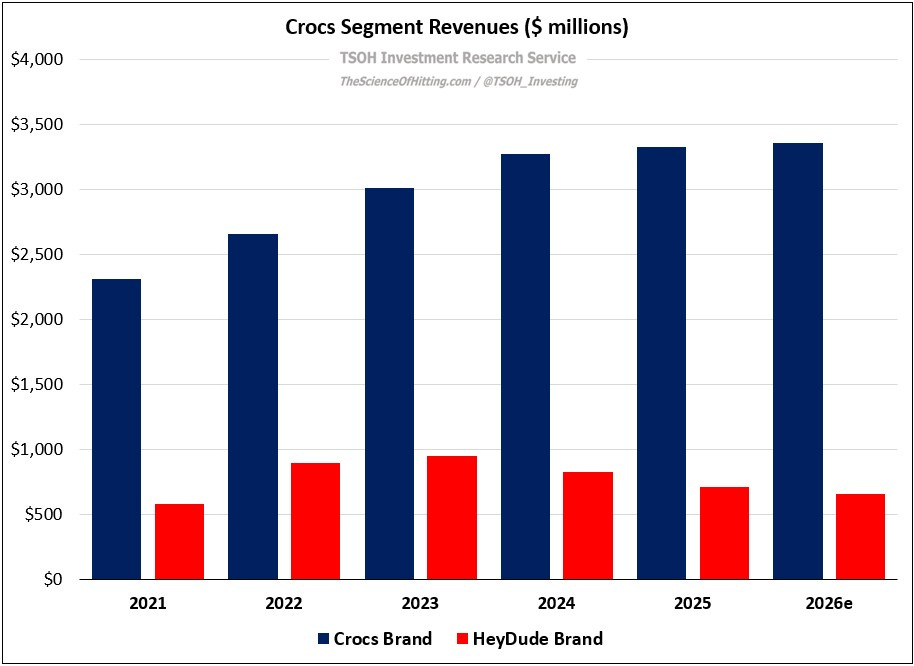

Monday’s post will be an update on Crocs (CROX), a company that I initiated coverage on in October 2025. The shares have struggled of late, with CROX trading at a mid-single digit P/E on FY26e. I’ll dig into recent trends at the namesake brand, along with an update on the HeyDude turnaround efforts.

As always, any resulting portfolio changes will be disclosed to TSOH paid subscribers before the trades are executed (100% portfolio transparency).

Have a great weekend!

NOTE - This is not investment advice. Do your own due diligence.

I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information presented in this report. Assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Projections are based on a number of assumptions, and there is no guarantee that they will be achieved. TSOH Investment Research is not acting as your advisor or in any fiduciary capacity.