DG: Closing The Gap

From “The DG Playbook” (March 2025):

“The source, severity, and expected duration of those pressures has been a topic of frequent discussion at TSOH Investment Research. My overarching conclusion is that despite the advances of certain competitors, most notably Walmart, Dollar General (DG) still meets a need for its core customer. At the same time, they did not keep up as the bar kept rising in an intensely competitive industry. That, in my view, is why the strategic shift on Dollar General’s unit growth is appropriate: management’s overwhelming focus needs to be on solidifying the base.”

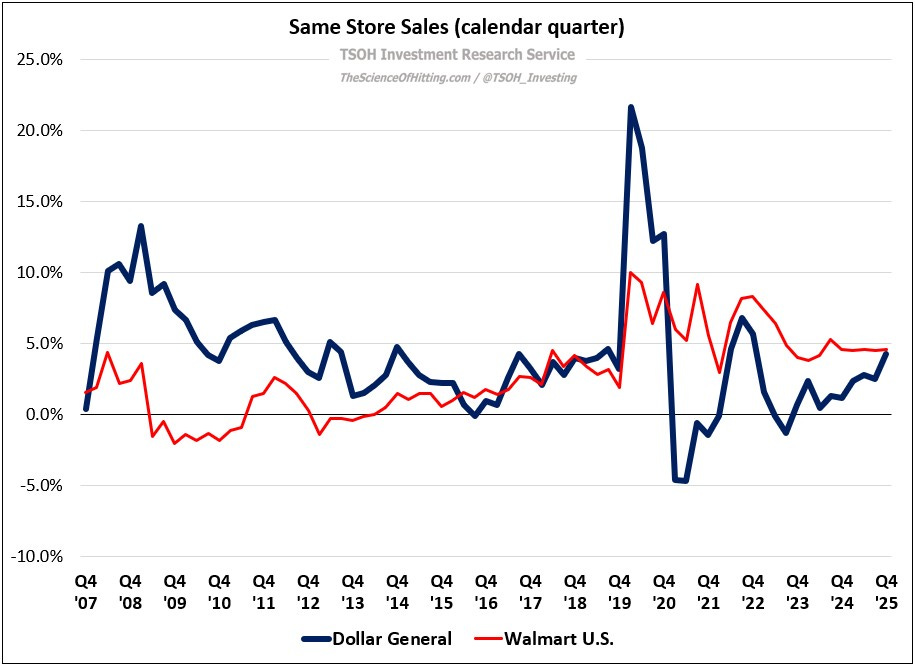

While the successful implementation of Dollar General’s “Back To Basics” strategy is evident in a handful of data points that we’ll cover today, my preferred metric is the same store sales comparison with Walmart U.S.: as you can see below, the relative SSS gap between the two retailers in the most recent calendar quarter was the narrowest that it has been in five years (a year ago, in Q4 FY24, the spread between the two was ~350 basis points).

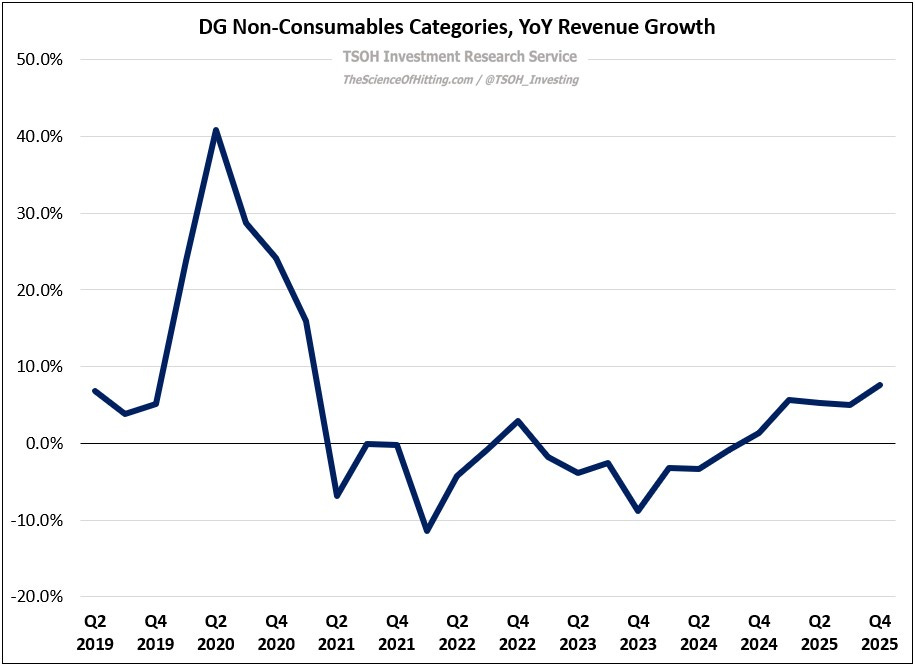

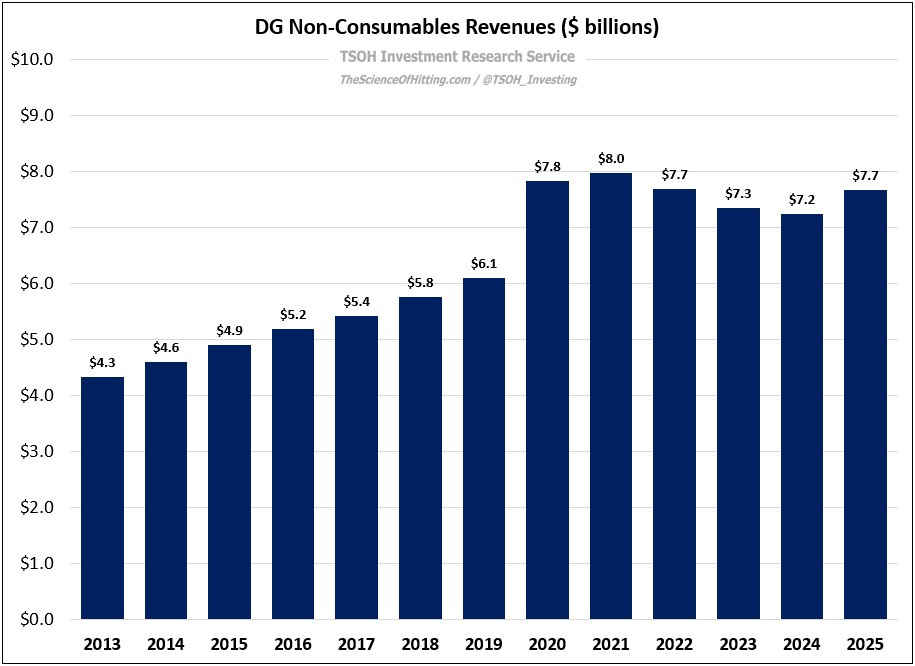

DG’s Q4 FY25 comps were +4.3%, which was led by nearly 3% traffic growth and gains across all product categories. The strong Q4 FY25 results were inclusive of high-single digit Non-Consumables revenue growth, led by Home and Seasonal – again, the best outcome reported by the banner in five years.

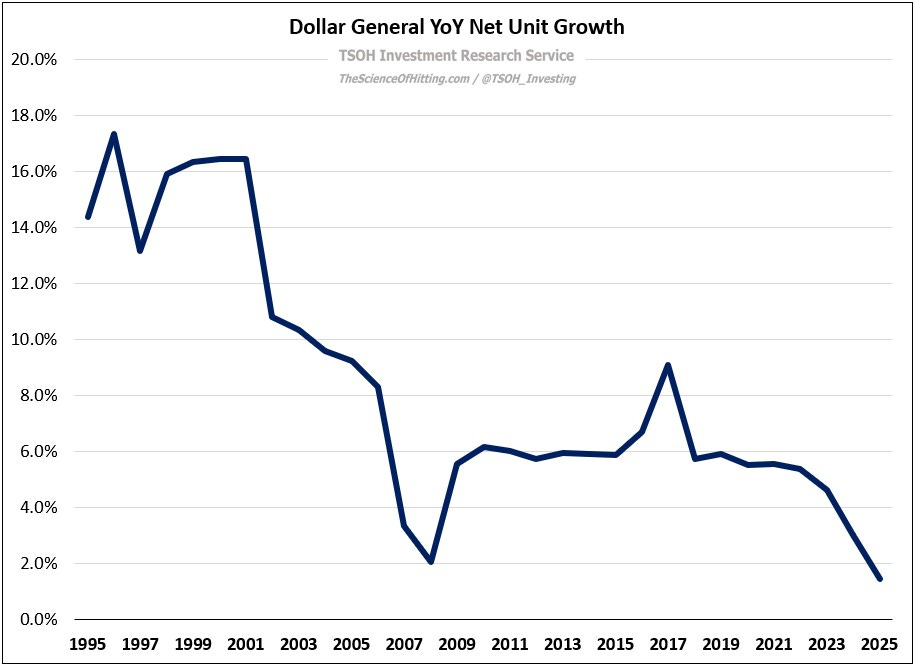

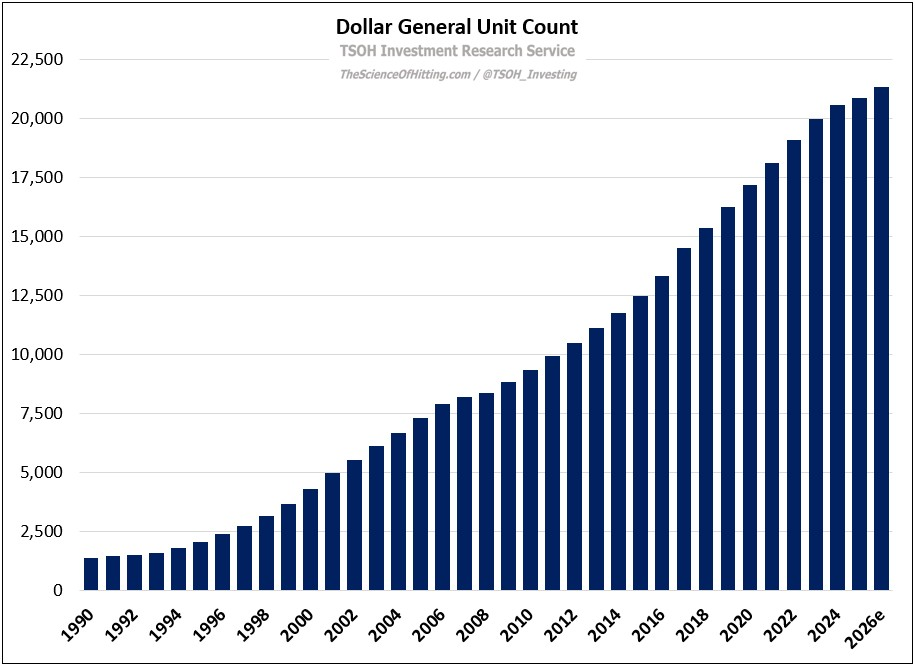

I believe these are signs of tangible progress amidst a shift in strategic focus. First, new unit growth has been deprioritized, with sub-2% growth in FY25 – the lowest unit growth rate (%) at Dollar General in at least three decades.