Fever-Tree: "A Pivotal Moment"

From “Fever-Tree: A Great Blueprint” (September 2025):

“One has to wonder what the future looks like for smaller competitors, particularly when Fever-Tree / Molson Coors (TAP) accelerate their marketing investments… With a strong and unique brand, leading value share, and an advantaged supply chain / distribution through TAP, Fever-Tree isn’t just a premium tonic / mixer brand; for a large number of consumers, it is becoming the premium tonic / mixer brand. (Optimism here should be tempered given the relatively small size of the U.S. mixers market; to sustain strong U.S. growth rates over the next 10+ years, Fever-Tree must win beyond tonics.)”

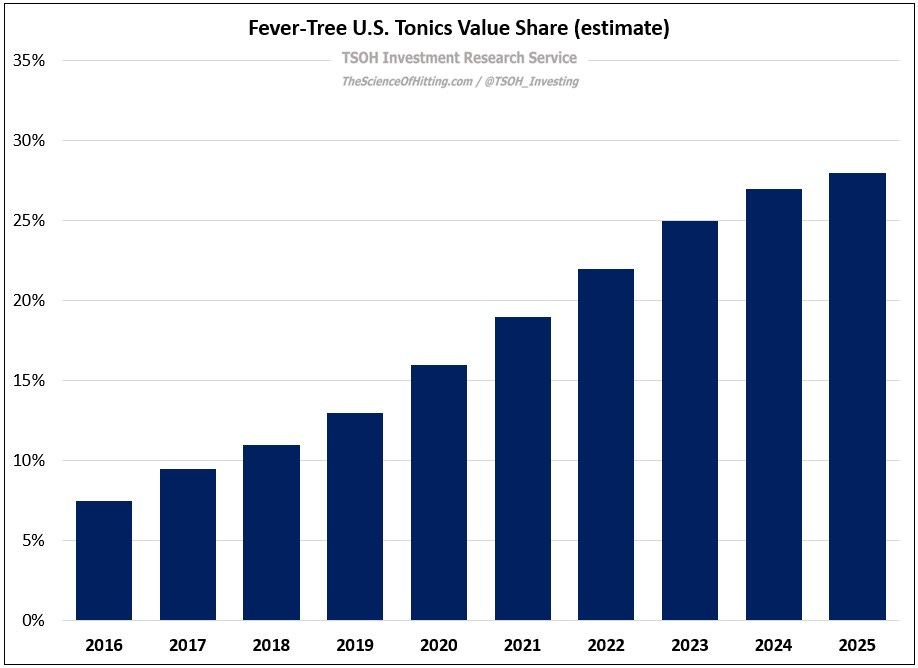

Despite navigating the transition to the Molson Coors distribution system, Fever-Tree reported another year of solid results in U.S. mixers, with its retail value share in tonics (Nielsen Total US xAOC) climbing to ~28% in 2025, up from a low-teens share pre-pandemic. While we don’t have financial data for smaller competitors, I think a recent product launch from Q Mixers – “Q Refreshers” – may be indicative of pressure faced within their core range.

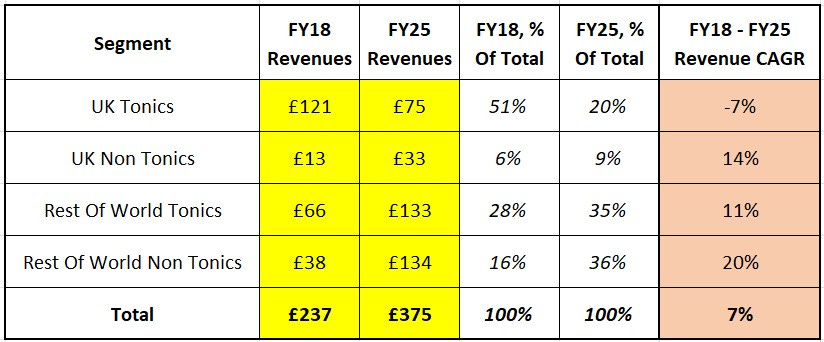

With that said, Fever-Tree continues its own brand extension beyond the core tonics and ginger SKUs, in the U.S. and around the world (most notably thus far in the UK). Group results over the past 5+ years were defined by the need to overcome headwinds from UK Tonics – a business which accounted for >50% of FEVR’s FY18 revenues, and which declined at a high-single digit annualized rate over the next seven years (~£121 million to ~£75 million).

The good news is UK Tonics have since shrunk to just ~20% of Fever-Tree’s revenue base. (In FY25, UK Tonics revenues declined ~6%, with UK Non-Tonics up ~6%.) The rest of the pie is a ~£300 million business that grew revenues at a mid-teens annualized clip over the past seven years, primarily due to the expansion of the non-Tonics range – starting with gingers, then followed by premium sodas / soft drinks, cocktail mixers, and non-alc RTD’s.

My investment is a bet on the long-term runway for the other ~80%.

This assumes long-term opportunities for the Fever-Tree brand will not be narrowly constrained to tonics or mixers; they are in pursuit of a much larger beverage TAM, and with good reason to believe that success is an attainable long-term objective. If I’m right about this, I believe that the equity is currently priced to generate attractive returns for investors over the next 3-5 years.