TSOH Weekly Roundup (06/26/26)

Welcome to another edition of TSOH Weekly Roundup.

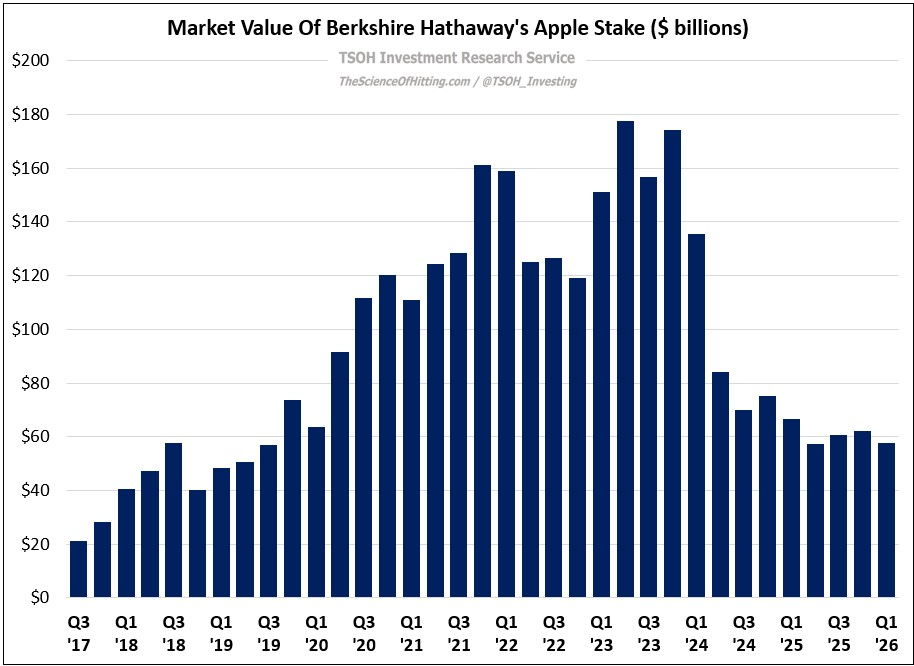

Chart Of The Week (from “The ‘Too Hard’ Pile”)

Three Notable Items

“Dollar Tree Announces Secondary Block Trade by Selling Stockholders and Share Buyback”

An interesting development: Mantle Ridge is preparing to sell the vast majority of its Dollar Tree stake (as a reminder, I’ve previously covered the history of Mantle Ridge’s involvement at DLTR). In addition, subject to the completion of the Mantle Ridge block trade, Dollar Tree will repurchase $500 million of stock, bringing year to date repurchases to at least $1.2 billion.

Dollar Tree CEO Mike Creedon: “This share repurchase reflects our commitment to disciplined capital allocation and our confidence in the long-term outlook for Dollar Tree. Our priority remains investing in initiatives that drive sustainable growth across the business, while maintaining a strong balance sheet and thoughtfully returning excess capital to shareholders.”

“Value Investing Legend Seth Klarman: Masters in Business”

A recent interview with Seth Klarman, which touches on a range of topics including the history of Baupost Group, investment lessons he learned over the decades, and how he’s navigating today’s AI-driven market environment.

On holding cash: “I would accept that I almost certainly made a mistake. Holding cash to that extent - there were times we had 30% cash or higher - was something that I viewed as valuable optionality. The problem is that optionality has not paid off very well for big swaths of time, particularly since 2008… We haven’t really had a serious downturn in almost two decades.”

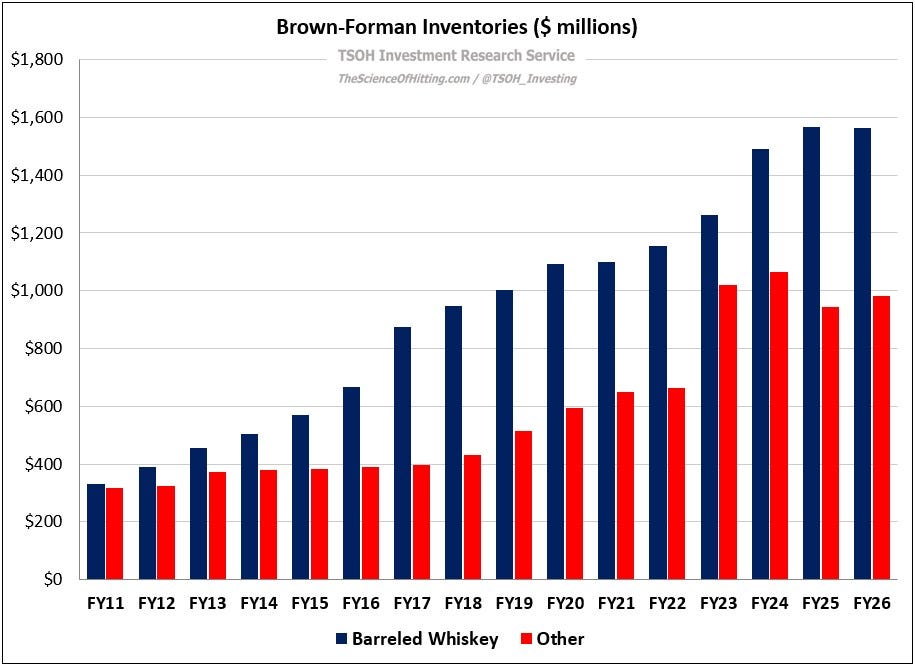

A discussion with Greg Hughes, the CEO of Suntory Global Spirits (the company behind American whiskey brands like Jim Beam and Maker’s Mark). With sustained end market pressure in the alcohol / spirits industry, and a supply glut that may impact premiumization and net pricing, I’m interested to see how companies like Brown-Forman will evolve in the years ahead - in terms of their strategy, but also as it relates to M&A / staying independent.

“You thought you were a genius in this industry [from 2010 – 2019] because you had a ~6% p.a. category revenue tailwind driven by premiumization, which caused margins to expand. You have an industry that built inventories and developed CapEx / OpEx around a growth algorithm of 6% - 8% topline growth with really good margins. It will resettle, after the transition, probably to ~3% global growth and still pretty good margins… If you’re a whiskey lover, then this is going to be the golden age of whiskey… I think you will see downward pressure on pricing as people have surplus inventory to move.”

TSOH Updates

Here’s the updated TSOH research list for the past six months:

Have a great weekend!

NOTE - This is not investment advice. Do your own due diligence.

I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information presented in this report. Assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Projections are based on a number of assumptions, and there is no guarantee that they will be achieved. TSOH Investment Research is not acting as your advisor or in any fiduciary capacity.