The "Too Hard" Pile

In late 2011, Berkshire Hathaway disclosed a ~$10.9 billion investment in IBM. When Warren Buffett revealed the new position on CNBC, Becky Quick asked, “You don’t buy tech companies; why have you been buying IBM?”

Warren responded with the following:

“Well, I didn’t buy railroad companies for a long time either… I’ve probably read the IBM annual report every year for 50 years. This year I read it and I got a different slant on IBM, which I proceeded to do some checking on. I just read it through a different lens… We went to our companies to see how their IT departments functioned and why they made the decisions they made, and I just came away with a different view of the position IBM holds within IT departments, why they hold it, its stickiness, and a whole bunch of things.”

Six months later, at the 2012 annual meeting, Warren and Charlie were asked whether the IBM purchase reflected a willingness to invest in other large tech companies, with the question specifically mentioning Google and Apple.

This was their response:

Buffett: “Well, Google and Apple are extraordinary companies, and they are huge companies with fantastic returns on capital. They look very tough to dislodge where they have their strengths. I would not be at all surprised to see them be worth a lot more money ten years from now, but I wouldn’t want to buy either one of them. I don’t get to the level of conviction that would cause me to buy - but I sure as hell wouldn’t short them either.”

Munger: “I think we can fairly say other people will always understand those two companies better than we do. We have the reverse of an edge, and we’re not looking for that. I don’t think that the same thing is true in IBM; I think IBM is easier for us to understand.”

Buffett: “The chances of being way wrong on IBM are probably less, at least for us, than being way wrong on Google or Apple. That doesn’t mean the latter two companies aren’t going to do, say, far better than IBM. We wouldn’t have predicted what would happen with Apple ten years ago, and it’s very hard for me to predict what will happen in the next ten years. They have come up with these brilliant products, but there are other people trying to come up with brilliant products, and I just don’t know how to evaluate people out there working in big companies or in garages, trying to think of something that will change the world the way [Apple] changed it.”

Munger: “And what do we know about computer science?”

Charlie added the following comment at the 2013 annual meeting: “We think BNSF will have a competitive advantage fifteen years from now, and with a high degree of confidence. We would never have that degree of confidence about Apple, no matter what their financial statements showed. It’s too hard.”

At the time, these statements seemed pretty unambiguous.

And then, just a few years later, they changed their minds.

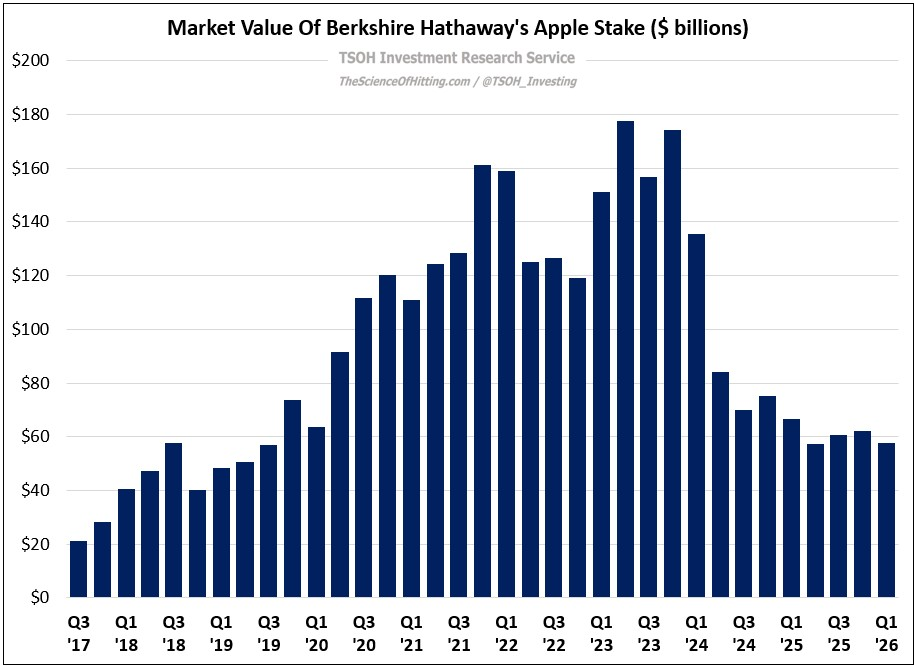

In 2016, Warren started buying Apple, following an initial investment in the company for Berkshire by Ted Weschler. By 2018, at which point Warren had finished buying, Berkshire’s cost basis was $36 billion. The stock delivered a >40% CAGR over the next 4.5 years (Q1 ‘19 - Q2 ‘23), leading to a position with a peak quarter-end market value of ~$178 billion, or >7x larger than the value of the Coca-Cola position – an investment that dates back to 1988, and a stock Warren has never sold a single share of. (That hasn’t been the case with Apple: the number of shares held has been cut ~75% since YE 2021.)

To summarize, Apple was a company / stock that Warren and Charlie clearly suggested was an unlikely candidate for investment – and then it became by far the largest equity position in Berkshire’s history, measured by its cost basis or its market value. (In Q2 2023, when the position value was nearly $180 billion, it accounted for more than 50% of Berkshire’s equity portfolio.)

And while I’ll spare you the comparable history on Google (Alphabet), we may be seeing similar developments, with the market value of Berkshire’s position in the company now up around $30 billion. No matter how Alphabet turns out, one thing is certain: Apple was a massive home run, and Berkshire investors should be very thankful Warren and Charlie changed their minds.

This example reveals an important lesson for fellow investors: the limitation of an overly restrictive and static “too hard” pile, specifically the risk of missing attractive investments within one’s circle of competence. (I touched on this in the Q4 2025 Portfolio Update, i.e. the need for soul searching among value investors like myself in productively responding to a changing world.)

Generally speaking, I think a “too hard” pile is a useful idea, particularly to help novice investors contextualize the border of their circle of competence. To use Peter Lynch’s phrasing, the first requirement in successful investing is “to know what you own”. But where the concept of a “too hard” pile risks becoming a net negative is when its application becomes overly rigid, to the point when the practitioner may not just be indifferent, but even starts to feel reassured, when they are unwilling to put in the time and effort to even try to understand companies and industries that could further develop their circle.

In security selection, one characteristic that’s highly correlated to inclusion in the “too hard” pile is a business in an industry subject to rapid change. The issue is when that determination becomes overly simplistic and static – for example, concluding that every company in the tech industry should be tossed in the pile - without due consideration for the risks and opportunities that come with change. (That consideration may also be accounted for through portfolio construction and position sizing.) Companies and industries are always changing; business managers and investors who don’t recognize that are likely to learn it eventually. As Warren noted at the 2014 meeting, “change goes on all the time, and it’s going on with all of our businesses.”

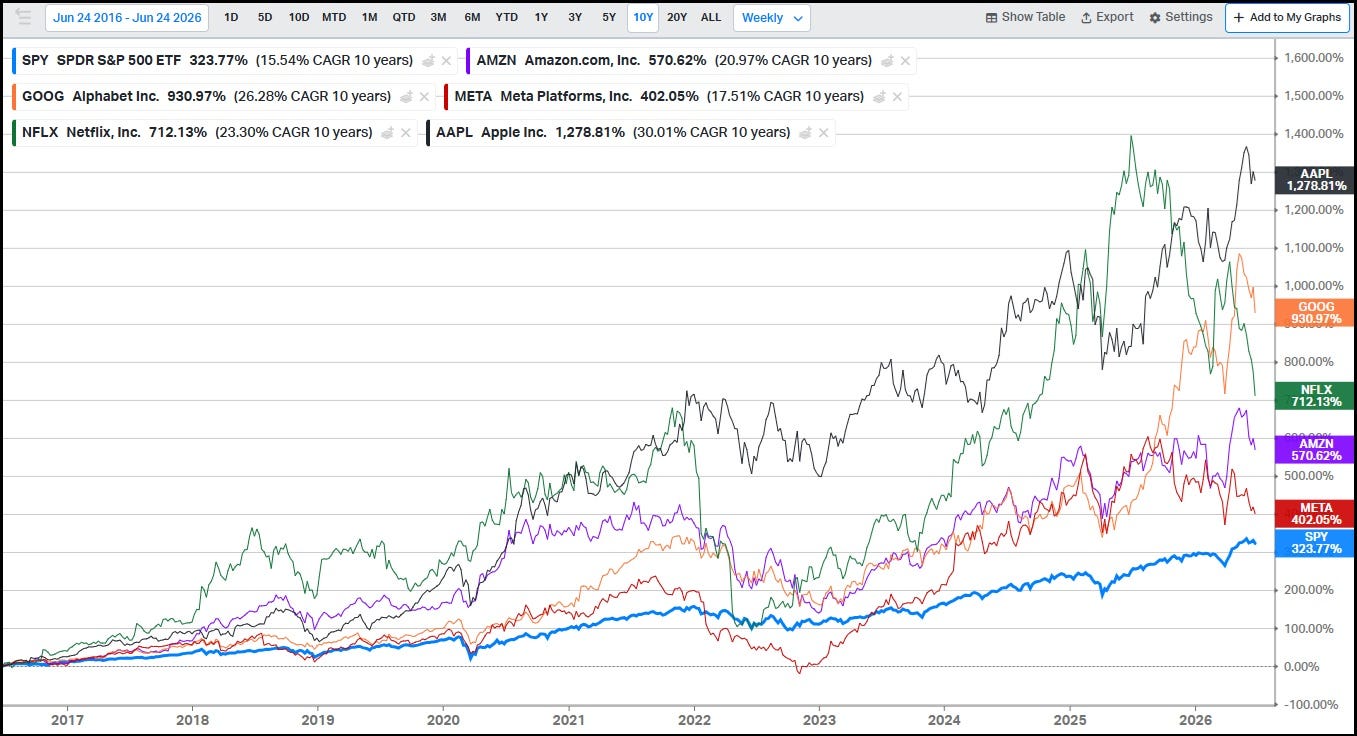

Over the past 10-20 years, tech companies like Amazon, Google, Meta, and Netflix have shown the importance of understanding this idea – in terms of capitalizing on opportunities, but also in avoiding risks that arise with change. These companies created massive value for shareholders over the past 10+ years, while simultaneously being involved in the disruption of high-quality companies and industries that were previously deemed resistant to change.

The general bias of value investors like myself is to be wary of and resistant to companies involved in driving change, while hoping to find undervalued securities among the legacy companies having that change imposed upon them. What can we do to nudge ourselves to a less restrictive opportunity set / “too hard” pile, while staying true to the tenets of our investment philosophy?

First, it’s critical to avoid being closed minded and dismissive in the initial analysis, to get lulled into a largely predetermined conclusion by pointing to “expensive” near-term valuation metrics without truly doing the research. Personally, that’s exactly what I did when I first looked at Netflix in the early-to-mid-2010s; it’s a decision that not only caused me to miss a potential NFLX investment, but I’d also argue it led me to not fully appreciate the challenges Disney would face in embarking on their DTC / OTT transition in the late 2010s (i.e. I may have concluded the right decision was to sell Disney if I truly understood the journey Netflix had been on over the prior decade).