Spotify (SPOT) Post-Mortem

“Not Just An Option, But A Necessity”

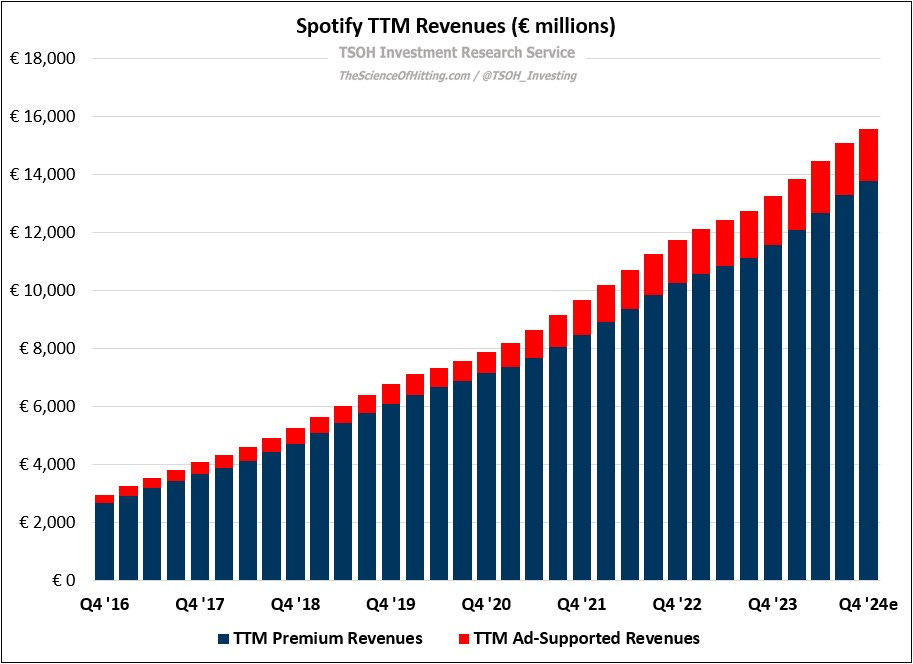

Shortly after TSOH Investment Research launched in April 2021, I made my first portfolio change: a 5% allocation to Spotify (SPOT). That was followed by additional purchases in May 2021, August 2021, February 2022, and March 2022. (All portfolio changes are archived on the TSOH Investment Research website under the “TSOH” tab, as well as by ticker.) My average cost basis was ~$217 per share. When I decided to liquidate the position in July 2023, my sale price was ~$147 per share. In total, I took a haircut equal to about one-third of my investment. If that wasn’t bad enough, the stock has since had an astounding run: SPOT closed on Wednesday at ~$477 per share, or ~120% above my cost basis. If I had managed to hold on through the wild volatility of the past three and a half years, it would’ve been a big winner.

The short summary of today’s discussion is that much of what I wrote in my initial assessment of Spotify appears to be directionally correct - more on that in a moment - but I totally fumbled how I navigated stock price volatility and near term developments at the company. The only thing worse than being wrong is being right… and still getting your hat handed to you by Mr. Market.

Why did this happen? What led to the >6x stock price increase for Spotify’s stock price from the November 2022 lows, and were there signals along that way that should have led me to rethink my prior conclusions? As I’ve worked through a post-mortem on the investment, I identified two key developments that fundamentally changed the story and business trajectory. I will discuss both of them below, along with thoughts on key takeaways and applicable learnings; it isn’t too enjoyable to revisit our mistakes, but it is critical for deriving the important lessons that should inform future portfolio decisions.

#1: Cost (OpEx) Efficiencies

In “Retain Optionality”, the July 2023 Spotify update, I wrote the following:

“Despite a fair amount of lip service paid to operating efficiency, the results thus far suggest there’s room for more forceful action. At the end of Q2 FY23, Spotify’s FTE headcount was down ~7% from peak levels at year end 2022 (and still up more than 100% since the end of 2019). By comparison, Meta has cut its headcount by more than 25% over a similar period of time. Given that Spotify is working under much tougher constraints than Meta (lower gross margins with limited room for improvement), they should be the one taking more aggressive action. In my view, this falls well short of the ‘intense focus on efficiency’ that management discussed on the Q4 FY22 call; if this business could get by with less than 6,000 employees in early 2020, it’s unfathomable to me why they couldn’t do the same today with ~7,500 FTE.”