Nike: Fighting Back

Note: Access all prior Nike (NKE) research on the TSOH website. Since the July 2022 initiation, I’ve penned seven dedicated post on Nike, with additional research examining others in the industry (ASO, DKS, HIBB, ONON, etc.).

“This is a difficult and challenging time for Nike… Our domestic footwear market is changing… Our long-held position is that our greatest asset is the NIKE trademark, which is increasingly taking its place as one of the great marks in the world. It is from this base that we attack the challenges facing us… Like many of our athletes who have faced adversity and won, we are fighting back… We believe that we can and will do better.”

Phil Knight, 1984 Nike Shareholder Letter

I have maintained a skeptical view on Nike (NKE) shares for the better part of the past four years. That conclusion was informed by the valuation, financial targets that were increasingly disconnected from the financial realities of the business, and a belief that this disconnect encouraged decisions which were subsequently putting the long-term health of the Nike brand into question.

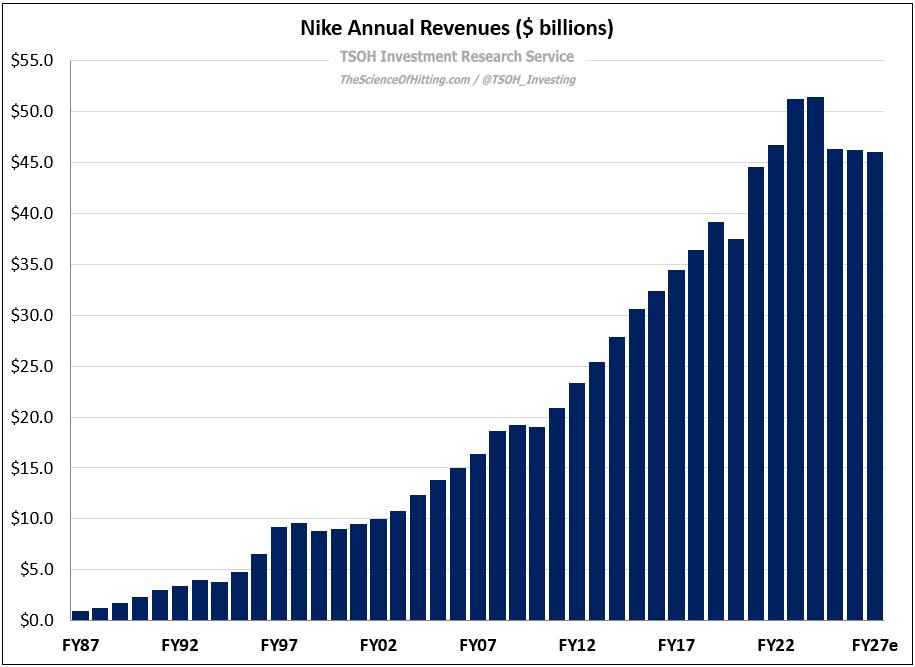

Thus far, this skepticism has been the right call. While the stock price is a crude measure, it helps frame the magnitude of Nike’s fading optimism among market participants: at ~$44 per share, the stock has declined by ~75% from the highs. It is trading at levels that were first reached in 2014.

A few years ago, management targeted double digit revenue growth and high-teens EBIT margins. As I’ll detail momentarily, today’s valuation now requires clearing a much lower bar. And while the competitive landscape has undoubtedly become tougher over the past decade, Nike management is tackling the key issues they needed to address (internal and external). Under the leadership of CEO Elliott Hill, one thing is clear: Nike is fighting back.