Convergence Calamity, Revisited

Note: Here are the links to prior TSOH research on CMCSA and LBRDA

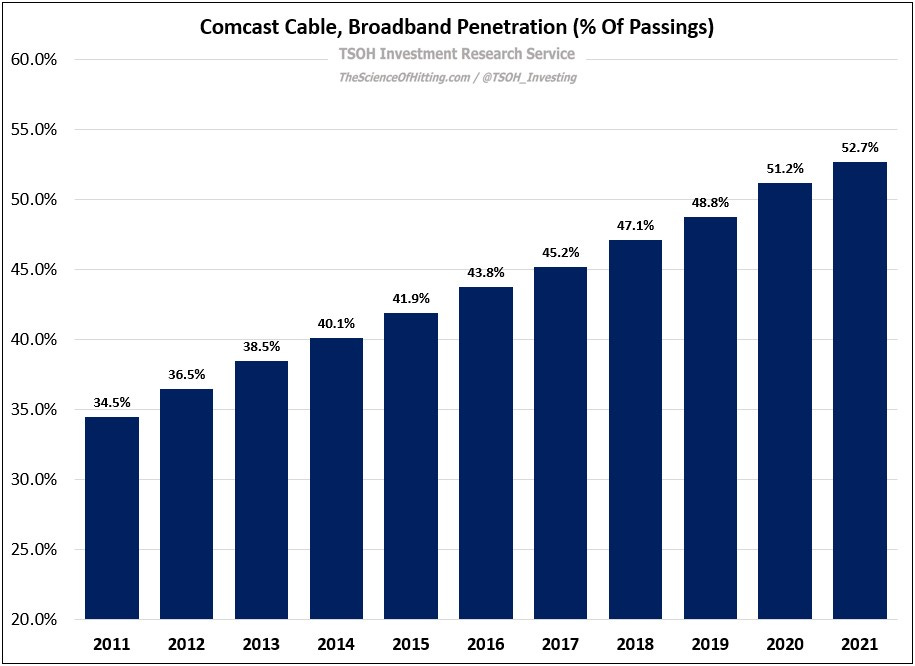

When 2021 came to a close, Comcast management could look back on the results of the prior decade with much to be delighted about. The broadband customer base had increased from 18.1 million in 2011 to 31.9 million in 2021 (+6% CAGR), with more than one million broadband net additions in every year during that period. While this result was helped by ongoing growth in homes and businesses passed - up 15% cumulative to 61 million - the larger factor was a significant increase in penetration (up from ~35% to ~53%).

That said, as the company looked ahead to 2022, it was already apparent that future growth was likely to be harder to come by; the combination of a significant pandemic-related pull forward of net adds, along with changes in the competitive landscape, suggested that the years ahead may look quite different relative to the results the company delivered over the prior decade.

In his opening remarks on Comcast’s Q4 FY21 call, CEO Brian Roberts said the following about the broadband business: “Within this environment, we will strike the right balance between subscriber acquisition - against a large and expanding addressable market - as well as long-term, profitable growth. We will evaluate every opportunity to increase our passings, even more so than we have in the past… We also will aggressively compete for market share through our strategy of bundling products around broadband, so that every customer in every segment has plenty of choice at the right price.”

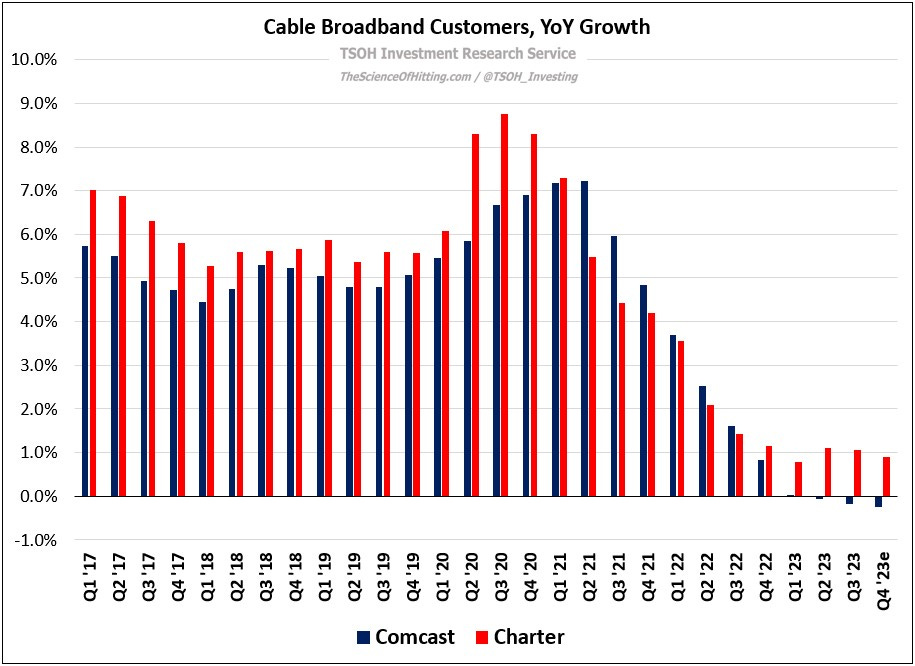

As we approach the end of 2023, the scorecard for the past two years is a mixed bag. While Comcast and (especially) Charter have done a good job on wireless, they’ve faced real pressure of late in broadband. For example, Comcast’s Q4 FY23 guidance suggests that they’ll end the year with ~32.2 million broadband customers – down 0.3% from YE FY22; on broadband penetration, that implies a rate that’s ~100 basis points lower than yearend FY21. As opposed to the mid-single digit volume growth reported from 2011 to 2021, the question has quickly become whether Comcast can grow core broadband customers at all (excluding gains from RDOF and the like.)

Directionally, the story is similar at Charter. While their management team has slightly differing views on the balance between volumes and rates (ARPU’s) in broadband, they are also facing headwinds: it now looks like they will fall well short of their FY23 goal of surpassing FY22’s +344k broadband net adds. While ~1% customer growth for FY23e is ahead of a comparable -0.3% decline at Comcast, Charter is also making some financial sacrifices to deliver that result; whether that trade-off is worthwhile is an open question.

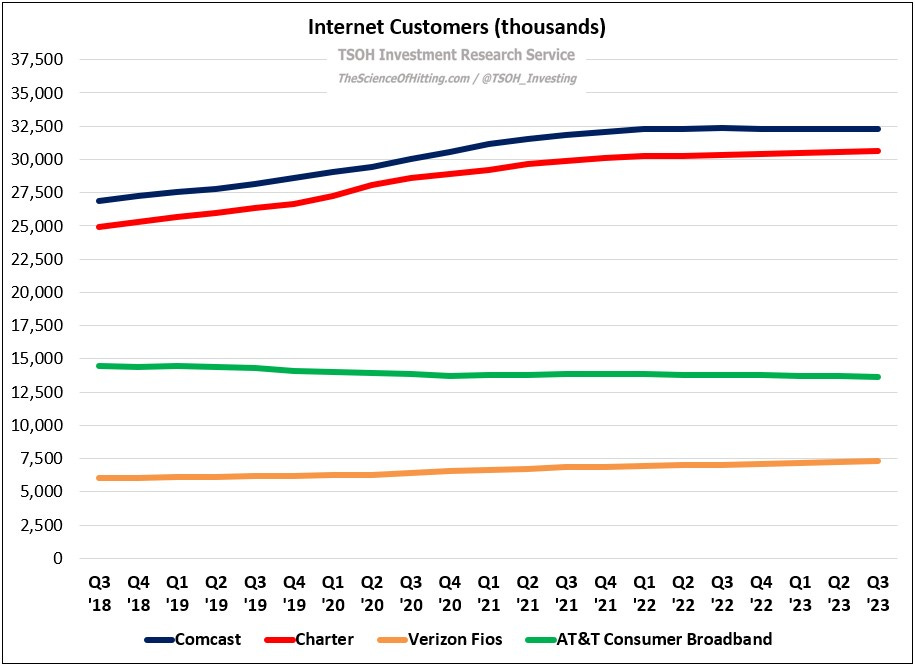

As we think about the cause of this shortfall, consider the following data for a few of the big names in the connectivity industry: Comcast, Charter, Verizon Fios, and AT&T Broadband. Five years ago (Q3 FY18), these companies had ~72.3 million internet customers. As of Q3 FY23, the total was ~83.9 million - with Comcast and Charter accounting for ~95% of the net adds. Even if we zoom in on the past 24 months, you’d still be hard pressed to conclude AT&T Broadband or Verizon Fios are the primary source of Cable’s problem.

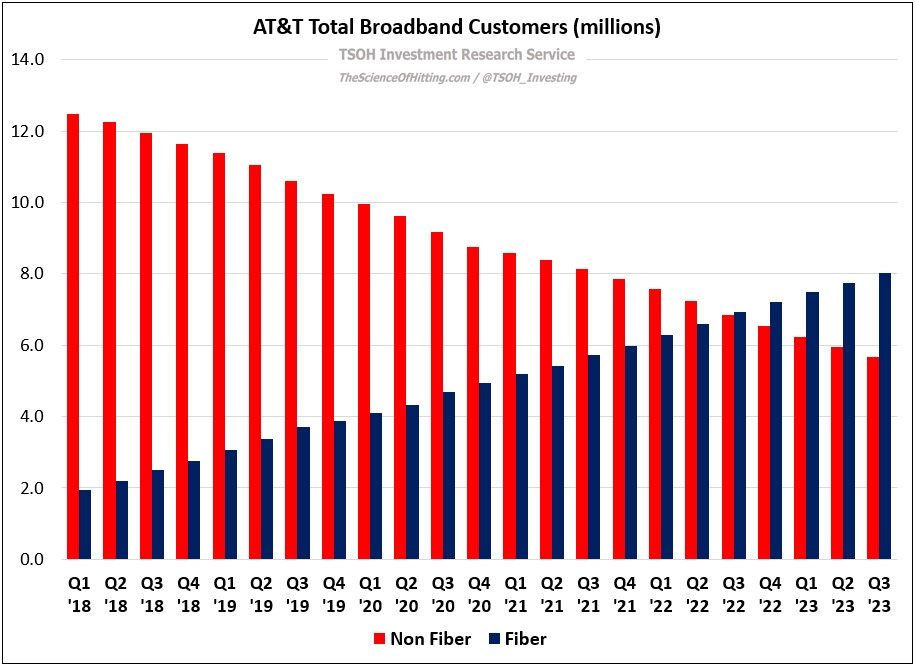

As you can see below for AT&T, that outcome reflects incessant pressure from the decline of their non-Fiber base. On a net basis, they have not been taking market share over the past five years. (Of course, if those two trends continue, the size of each bucket will be very different within 2-3 years.)

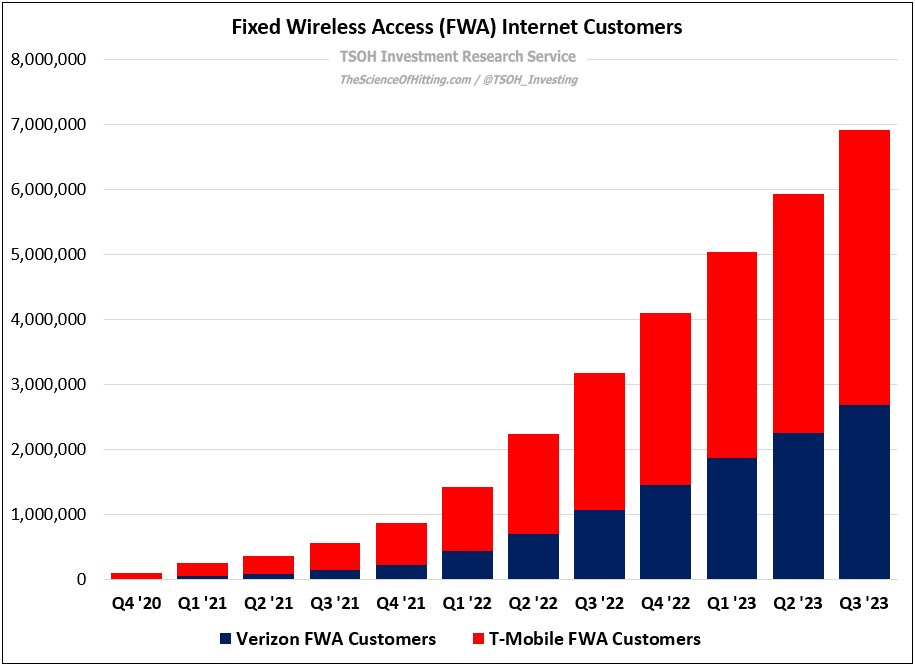

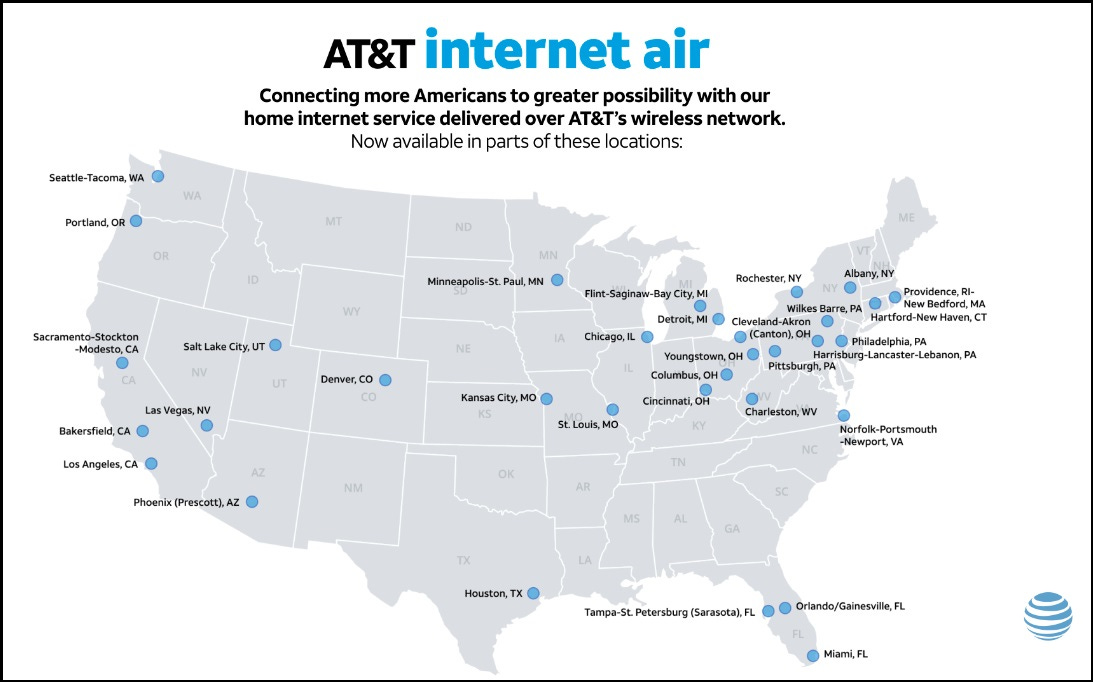

Contrast that with the results for another “competitor”: fixed wireless access, or FWA. As you can see below, Verizon and T-Mobile have collectively added nearly seven million FWA customers over the past three years (VZ FWA customers are not included in the Fios calculation). In addition, AT&T entered the FWA market in August 2023 with Internet Air, which quickly added ~25k customers. As noted on the company’s Q3 FY23 call, it will be a “targeted catch product” for copper / DSL customers (“typical download speeds between 40-140 Mbps”). It is available for $55 per month, or just $35 per month for AT&T customers with eligible wireless service; that compares to a non-Fiber monthly ARPU for AT&T Broadband in Q3 FY23 of $60 per month.

In summary, I think there’s reason to believe cable’s incremental net add headwinds are largely attributable to FWA, not Fiber. As we look ahead, I think two key questions need to be answered: (1) What are the competitive dynamics between FWA and Cable? (2) Is FWA a short-term phenomenon, or will it have a larger / longer lasting impact on U.S. household connectivity?

Competitive Dynamics

Is Cable a superior value proposition for customers than FWA? The somewhat uncomfortable answer, in my opinion, is that it depends.

First, note the relatively unimpressive AT&T Internet Air speeds cited earlier; while T-Mobile offers faster FWA speeds than AT&T - “typical download speeds between 72 - 245 Mbps” – it still falls well short of what Cable customers receive: as noted on Comcast’s Q3 call, ~70% of customers now take 400 Mbps or higher. (When I wrote about this topic in November 2022, T-Mobile’s website said typical download speeds were 33 - 182 Mbps.)

Whether those speeds are necessary is another question (“the benefits of paying for more than 100 megabits a second are marginal at best”). Consider one notable use case: Netflix’s speed recommendations state that 15 Mbps is sufficient for streaming UHD 4K video. This points to the uncomfortable answer mentioned above: there may be a large number of households where FWA is “good enough”, especially if it means that they can pay $25 - $35 per month instead of $60 - $70 per month. (That argument is supported by NPS scores, which are considerably higher for FWA than for Cable companies.)

The other consideration on competitive dynamics is where FWA competes. Consider this July 2022 comment from Comcast Cable CEO Dave Watson: “With fixed wireless… they’re a little bit more rural… but it's kind of across the board. When you have this launch phase at scale, you see it a little bit all over.” As opposed to solely attracting users in rural markets, FWA seems to have broader appeal. As an example, the list of AT&T Internet Air markets includes Chicago, Denver, Los Angeles, Philadelphia, and Seattle (this is the wireless company that has been most adamant against the broad use of FWA). In addition, as T-Mobile CEO Mike Sievert noted in May 2023, “Last quarter, 40% of our FWA gross additions came from smaller markets and rural areas” – with about 50% of FWA adds coming from Cable. At Comcast and Charter, FWA competitive dynamics are typically framed around network capacity constraints / trade-offs and speed limitations. But even if FWA proves to be a “substandard and temporary” competitor, that doesn’t provide much solace as it takes a few million customers per year in the interim – especially if we still have another two-plus years ahead (and maybe more).

TAM and Sustainability

T-Mobile’s management team has been consistent on their FWA customer growth targets since early 2021: “we will reach seven million to eight million customers by 2025”. Including Verizon, which expects to attract four to five million FWA customers by 2025, the total is ~12 million FWA customers.

Reaching the midpoint of their combined goal would result in roughly 2.3 million net FWA Home Internet customers adds annually, on average, through the end of 2025. What about after 2025? For T-Mobile, the business case for FWA has always been framed around the use of fallow capacity. While management continues to explore economically viable ways to grow this business beyond that initial target, I think the reality is that selling the same bits for a fraction of what you’d charge a wireless customers suggests that they still haven’t figured out a direct answer (said differently, you can’t charge Home Internet customers ~$25 per month with that price locked in). That said, I think there’s a decent possibility that T-Mobile will find a way to justify the math, especially if they see material premium wireless (Magenta Max) upsell and / or churn benefits on bundled customers. (As Altice noted on their Q3 FY23 call, bundled customers have churn reductions of more than 20% relative to their traditional internet customers; for each connectivity company, that benefit will influence what they require on the standalone economics.)

Verizon’s view on FWA seems more expansive than T-Mobile’s. While the commercial roll-out of FWA was delayed for a few years, they’ve publicly discussed this opportunity since 2016. Strong results have proven more consistent as of late, with TTM net customer adds in Q3 FY23 of ~1.6 million. As it relates to their future ambitions for FWA, here’s some recent commentary from CEO Hans Vestberg and CFO Anthony Skiadas: “There's clearly demand for FWA. The network team is building way beyond the four to five million target… We see a lot of opportunity… Assumptions changed on FWA because our technology has improved more than we thought, which means that we can take on even more capacity. We are only in the first inning on the software improvements and our optimization of the network… We still have a lot of technology evolution, so we can serve even more customers [over 4-5 million] with better performance and more capacity.”

Conclusion

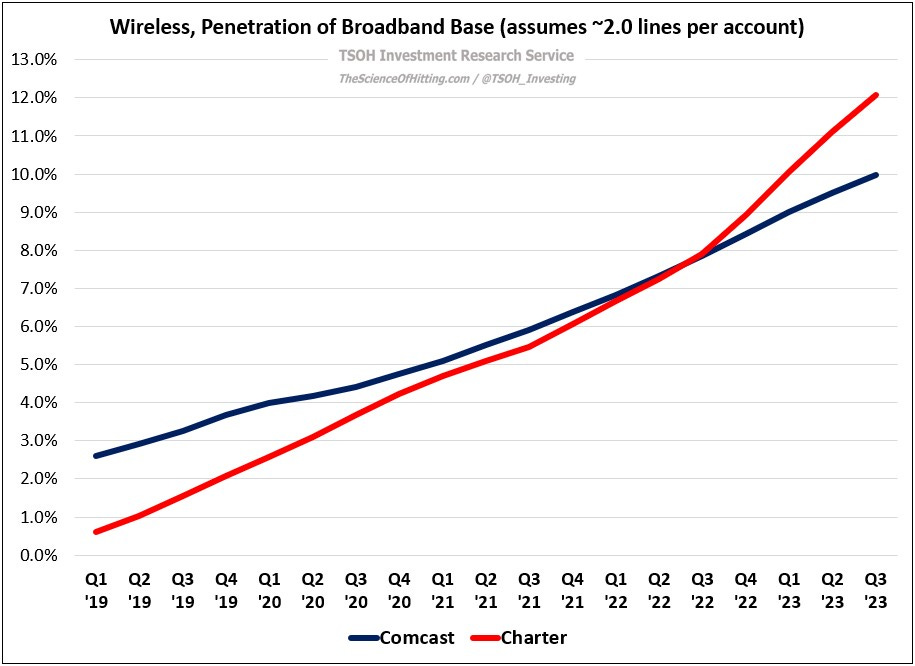

I continue to believe Cable has a compelling opportunity in connectivity, particularly as a result of the perpetual MVNO agreement (as you can see below, wireless penetration is rising quickly at both companies). I’m still convinced Cable remains well positioned to effectively compete through connectivity bundles, which will drive much higher wireless penetration.

The problem, as I see it, is that competition is intensifying.

My fear is that AT&T, Charter, Comcast, T-Mobile, and Verizon are moving closer to the “convergence calamity”. Cable may remain the best house on the block – but they’re living in a tough neighborhood. By way of example, consider Verizon’s first FWA residential roll-out in October 2018; the monthly cost was $50 for Verizon customers and $70 for non-Verizon customers. Contrast that with the $25 per month being charged for new Home Internet customers in June 2022 (it was increased ~$10 during Q3 FY23). Even if the FWA customer gains are temporary, it’s still a major headwind to short-term Cable volumes. On that point, this is one key area I’ve changed my views: I am not convinced T-Mobile and Verizon will stop going after new FWA customers (beyond their 2025 targets), even if it presents somewhat uncertain standalone economics; one way or another, I think they’ll find some rationale to keep going after those incremental customers. (Think about this comment from AT&T COO Jeff McElfresh, in response to a question about FWA growth at T-Mobile and Verizon: “If all I had was a wireless network, if I didn’t have scaled physical infrastructure, I might have no choice but to leverage my wireless spectrum portfolio to grow my business.”)

In summary, I’ve become more worried about incremental competitive intensity across the connectivity industries, most notably as it relates to high fixed costs / CapEx needs, operating leverage, and financial leverage. In addition to the long-term threat from Fiber, technological improvements have made FWA a real competitor to broadband for some percentage of U.S. households (as a reminder, T-Mobile started with a goal of delivering FWA speeds of “up to 50 Mbps”). Given that conclusion, I struggle to confidently state Charter and Comcast will continue to grow core broadband subs at a reasonable clip (anywhere close to one million net adds per year, which at their current scale would equate to ~3% annualized volume growth).

In my mind, that suggests the Cable investment thesis is no longer valid. The stocks may work from here, but I think they’ve moved even further towards an ARPU / capital returns driven total return algorithm. Personally, that’s a setup that I’ve grown cautious of over time. (Said differently, I’ve seen how these situations can become value traps when the plan goes awry.)

For that reason, I’ve decided to sell Liberty Broadband and Comcast.

This decision wasn’t made lightly. That said, I do want to note one important consideration that ultimately played a role in this verdict: I’m starting to see a number of more interesting opportunities arise in pockets of the market.

Given that I started trimming Comcast earlier this year, it’s probably not too surprising to hear that I continued to view it as a potential funding source (particularly after the negative incremental data in Q3 FY23). The decision to sell Liberty Broadband was more difficult for me. I think there’s a lot of merit to their strategy, and still believe it could work well over the long run. That said, I ultimately concluded those funds have a better use elsewhere at this time. Over time, we’ll see if Cable’s results provide reason to revisit a potential investment.

I’ll send another update after the market close (at 5pm eastern time) outlining the specific portfolio changes that I will execute on Tuesday morning.

NOTE - This is not investment advice. Do your own due diligence. I make no representation, warranty, or undertaking, express or implied, as to the accuracy, reliability, completeness, or reasonableness of the information contained in this report. Any assumptions, opinions, and estimates expressed in this report constitute my judgment as of the date thereof and are subject to change without notice. Any projections contained in the report are based on a number of assumptions as to market conditions. There is no guarantee that projected outcomes will be achieved. The TSOH Investment Research Service is not acting as your financial advisor or in any fiduciary capacity.