Cable's Strategic Vision(s)

An update on Comcast and Charter (Liberty Broadband)

TSOH Weekly #3: Comcast (Peacock)

The past few years have presented a number of challenging questions for cable investors. The list has included the structural decline of linear TV in the United States, COVID-related impacts on the timing of broadband customer growth, and competitive threats from fiber and fixed wireless, to name a few (the list is even longer for Comcast given its ownership of NBCU and Sky).

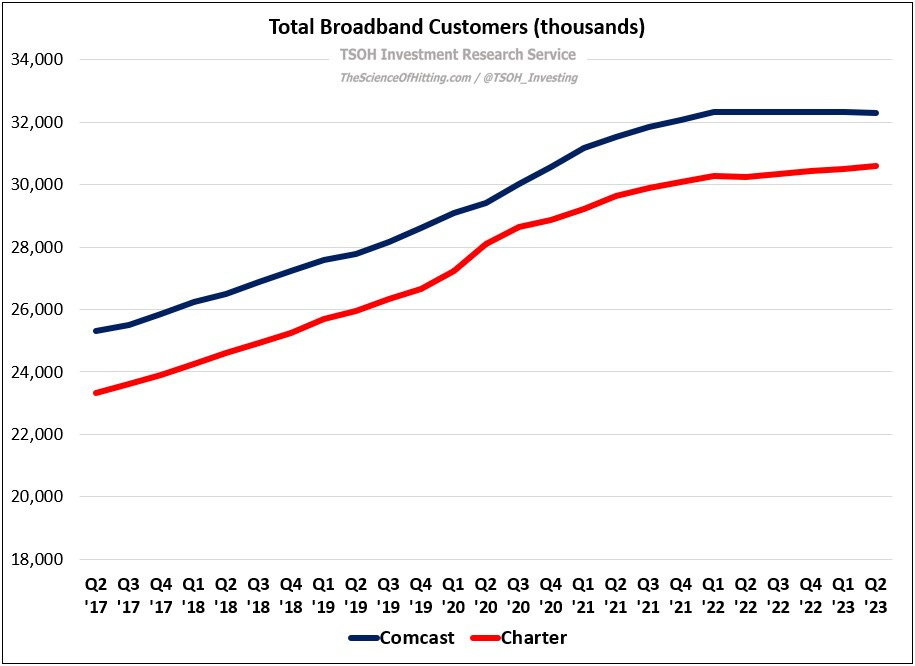

That said, Comcast and Charter have generally done a reasonable job navigating these pressures, with each company now serving more than 30 million broadband households. In addition, they both retain a very valuable strategic asset through their perpetual MVNO agreement with Verizon.

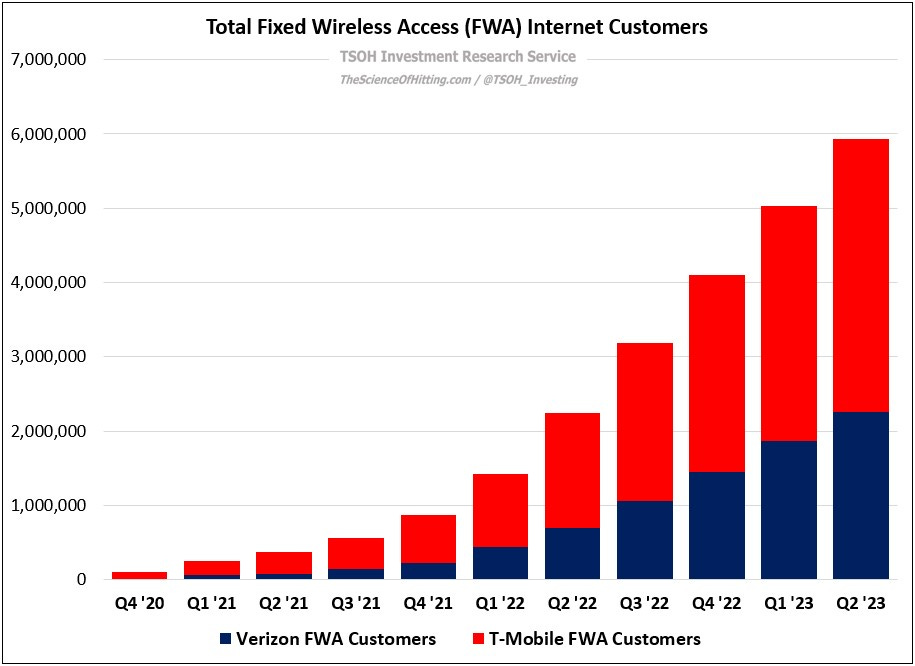

In light of these developments, and particularly as a result of the growing importance of the wireless business, my conclusion is that there has been a meaningful change in the cable investment thesis since 2020. While there’s always the risk of thesis creep in these situations, I think there’s good reason to believe the cable companies are somewhat uniquely positioned to skate to where the puck is going (their converged connectivity offering is a win for customers and shareholders). The biggest question, in my mind, is how aggressive they’re willing to be in pursuit of this long-term opportunity.

Comcast

The distinction between the results at Comcast Cable and Charter that I’ve discussed in recent quarters continued in Q2. At Comcast, the company’s Connectivity & Platforms segment reported 4% YoY EBITDA growth, to $8.3 billion, on flat revenues (margins +170 basis points YoY to 41.0%). Within those results, the domestic broadband base declined marginally from the year ago period (-0.1%, to 32.3 million customers), with the lack of volume growth offset by a nearly 5% increase in ARPU’s. In addition, as noted on the company’s earnings call, this was the second consecutive quarter that every expense line in the segment declined YoY (except for direct product costs); said differently, management is clearly saying to shareholders that lower spending on marketing, customer service, etc., is a desirable outcome. All else equal, I would agree – but the part that I’m unsure about is whether “all else equal” is an appropriate assumption, particularly over the long run.

As it relates to the composition of growth in the quarter (rate vs volumes), this comment from Comcast Cable CEO Dave Watson on broadband ARPU’s was noteworthy: “I think a critical factor for us is tier mix. One-third of our base is on a gigabit or higher, and 75% of our base is on 400 megabits or higher - that definitely impacts the overall ARPU.” (To provide some context for those figures, Watson disclosed in July 2018 that 75% of the base had speeds of 100 megabits or higher.) As I think about the impressive FWA growth reported at T-Mobile and Verizon over the past 2-3 years, the data shared by Watson gives me further confidence that the combination of rising speed and usage demands by customers will limit its long-term applicability to a small percentage of use cases (and on that point, I think you can interpret this comment from TMUS CEO Mike Sievert as saying that the economic viability of FWA at today’s prices is largely dependent upon fallow capacity).