"A Position Of Strength"

Some thoughts on the DKS / FL deal

From “The House Of Sport” (January 2025):

“With research completed on Academy, Dick’s, Hibbett, Nike, and On, I’ve developed a clearer picture of how the industry evolved over the past 10-15 years. It has helped to illuminate why Dick’s strategy has been so effective: they invested to improve the in-store experience - a value add for customers and suppliers like Nike and On… House of Sport and Field House will further Dick’s ability to effectively compete in an evolving retail landscape; they succeeded in creating the format that could put a traditional Dick’s store out of business… Like Home Depot after the financial crisis, Dick’s shifted their focus from unit growth to perfecting the base… With clear capital allocation priorities, this could become an interesting setup if we see a period where Mr. Market questions the company’s sustainability.”

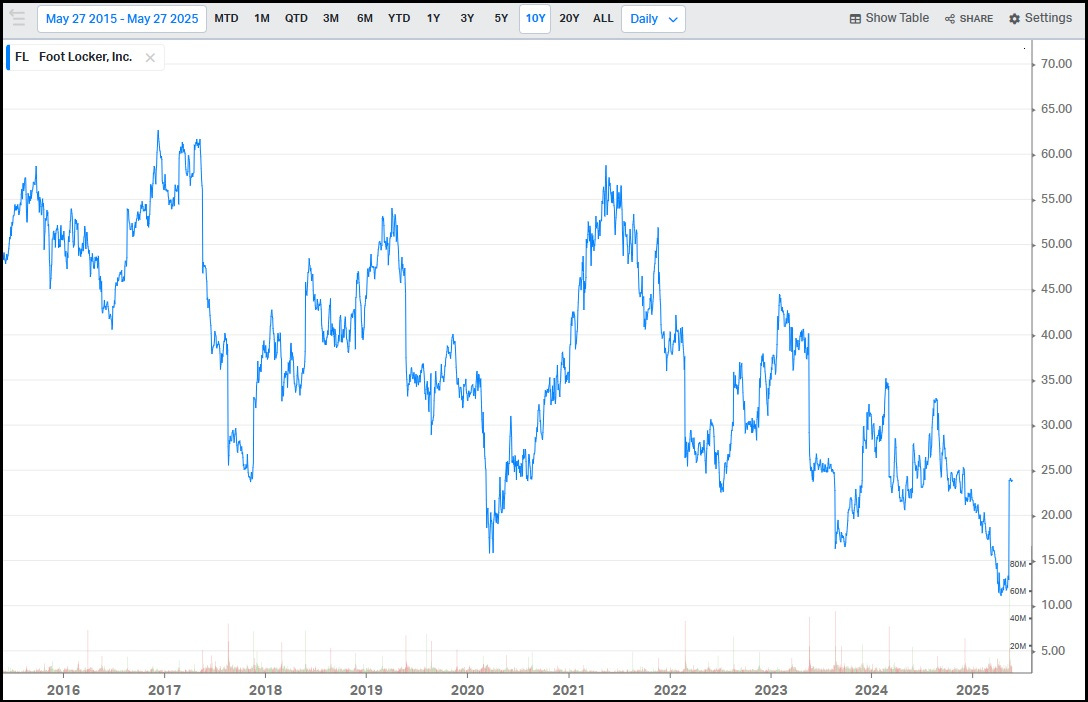

In the four months since that was written, Mr. Market has lived up to his end of the bargain: at $177 per share, the stock price has fallen by >20% year to date. While the initial move downward was outside of management’s control, the more recent decline was self-inflicted: on May 15th, Dick’s announced the ~$2.4 billion acquisition of Foot Locker. FL shareholders can elect to receive $24.00 in cash per FL share - a roughly 85% premium to where the stock traded prior to the announcement - or 0.1168 shares of DKS stock per FL share (with DKS at $177 per share, the equity option is valued at ~$20.7 per FL share). As you can see below, even with the >80% pop on the deal, this transaction will conclude a dreadful decade for Foot Locker shareholders.

The quote from “The House Of Sport” spoke to a management team with a clear long-term strategic vision for their business, along with straightforward capital allocation priorities. The Foot Locker deal, at least in the near term, has thrown a wrench in the gears of the DKS thesis. This wasn’t lost on management, who clearly appreciated that this deal was likely to raise some eyebrows in the investment community. In explaining their rationale for the acquisition, Ed Stack argued on the deal call that this isn’t new territory: