Tractor Supply: Old Dog, New Tricks?

From “The ‘Life Out Here’ Retailer” (April 2023):

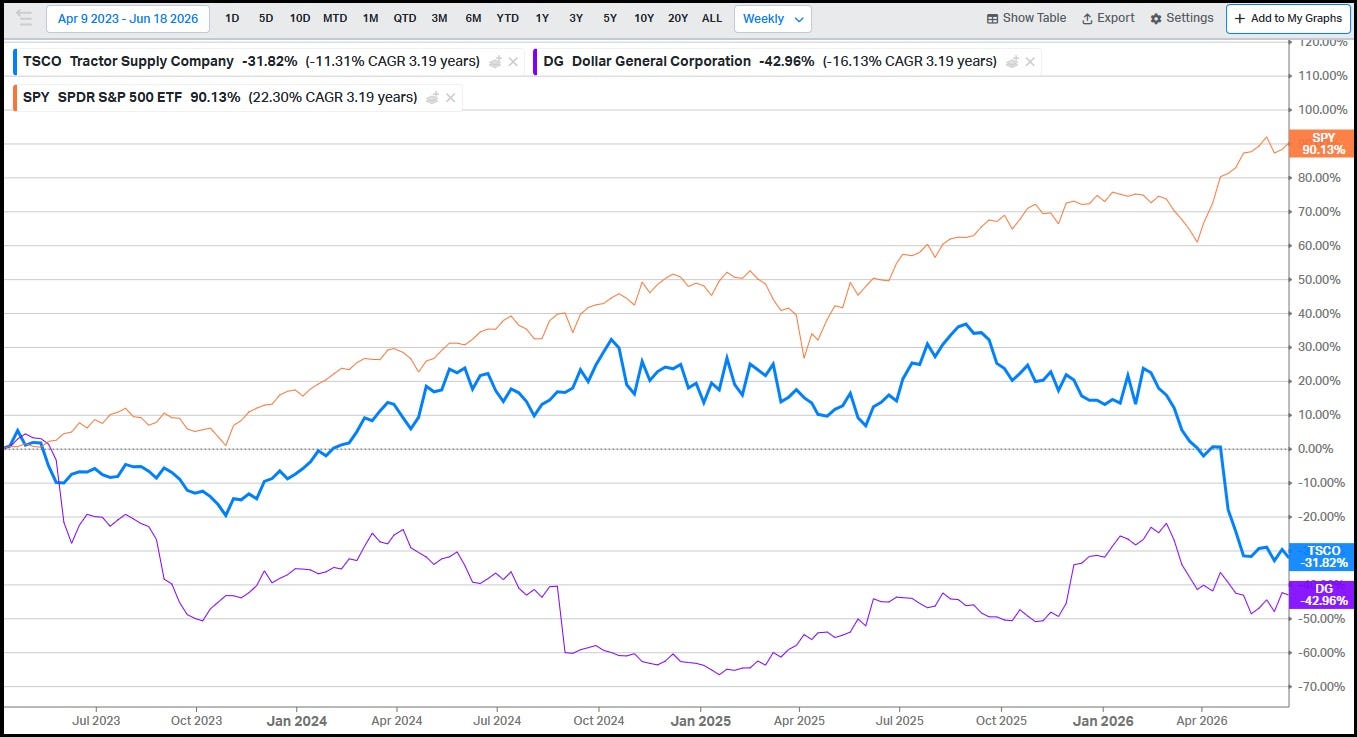

“There’s no question Tractor Supply has proven to be a fantastic long-term investment, with the stock price up ~25x over the past 15 years… As I think about a potential investment, it comes down to opportunity costs: is Tractor Supply likely to be a better long-term investment than Dollar General?”

While TSCO outperformed DG over the ensuing three years, it has been a difficult stretch for both companies. As you can see below, DG ran into trouble a few years ago, and has fought to regain ground since. TSCO, on the other hand, just recently fell into Mr. Market’s disfavor: the stock, which peaked at ~$64 per share in August 2025, is down >50% over the past ten months.

I view the primary role that DG and TSCO serve for core customers in a similar light, which I’d broadly define as rural consumables retailing. They win by providing a compelling balance between small box convenience and value - the right assortment, in-stock, and sold at competitive prices. But while Dollar General is primarily focused on selling consumables for people, Tractor Supply is primarily focused on selling consumables for animals and for pets (that isn’t to say it’s the only role they each serve, but it’s an important one).

I believe that DG’s lagging stock price has presented an attractive investment opportunity. Does the same idea apply to Tractor Supply, or is its recent stock price decline an appropriate reflection of evolving competitive dynamics?