Nike: Conditioning Phase

Note: Access all prior Nike (NKE) research on the TSOH website.

From “Nike: Fighting Back” (April 2026):

“While the near term picture is dominated by a barrage of financial pressures – the Classics pullback, China struggles, tariffs, etc. – I think these insiders have bought Nike shares because they believe the long-term trajectory for the business and the brand is much improved given the changes that have been implemented under Elliott Hill’s leadership over the past 18 months…”

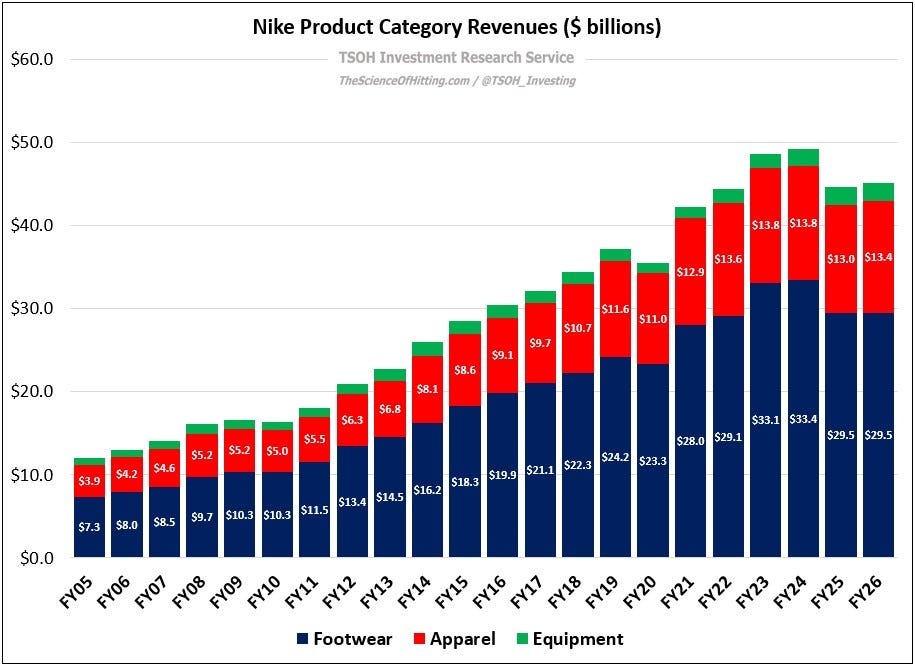

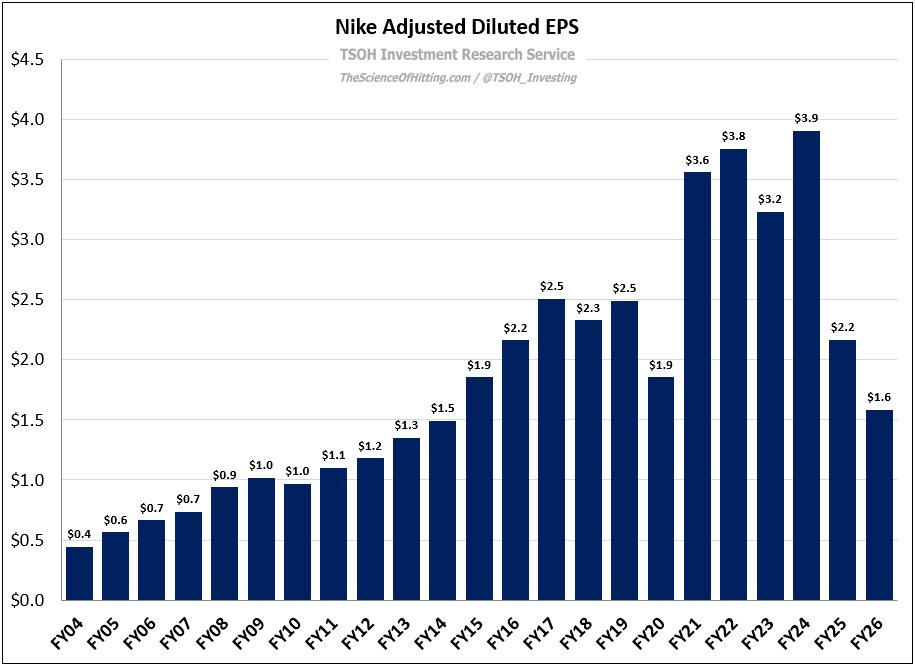

From a financial perspective, FY26 was a terrible year for Nike.

Revenues of ~$46.4 billion were nearly $5 billion lower than three years earlier, adjusted EBIT margins were down by half compared to the trailing ten-year average, and adjusted EPS fell to levels first eclipsed in FY15.

But today’s results are largely reflective of yesterday’s mistakes.

I believe that Nike is heading in the right direction under CEO Elliott Hill’s leadership, but it has required meaningful change. One notable development has been the >$4 billion revenue reduction from their classics footwear franchises, with roughly half of that impact realized in FY26; this resulted in minimal Footwear revenue growth for Nike over the past five years, a product category that historically drove mid-to-high single digit per annum (%) gains.