Floor & Decor: Awaiting Normalization

From “A More Normalized Environment” (September 2024):

“I continue to be surprised by Mr. Market’s willingness to look past Floor & Decor’s near term challenges. To be clear, I remain confident on the long-term opportunity that they are pursuing, as well as their competitive position. But I struggle to come to an estimate of normalized earnings power that would support today’s price – particularly if you believe we’re unlikely to get there anytime soon… Given recent commentary from management, I think it’s safe to assume they are not of the opinion that market tailwinds are right around the corner. If that’s the case, then the above financial model will need to be tweaked (once again). It follows downward revisions over the past 12-24 months - which Mr. Market has not exhibited too much (any) concern with so far. If it continues, we will see if Mr. Market maintains his indifference.”

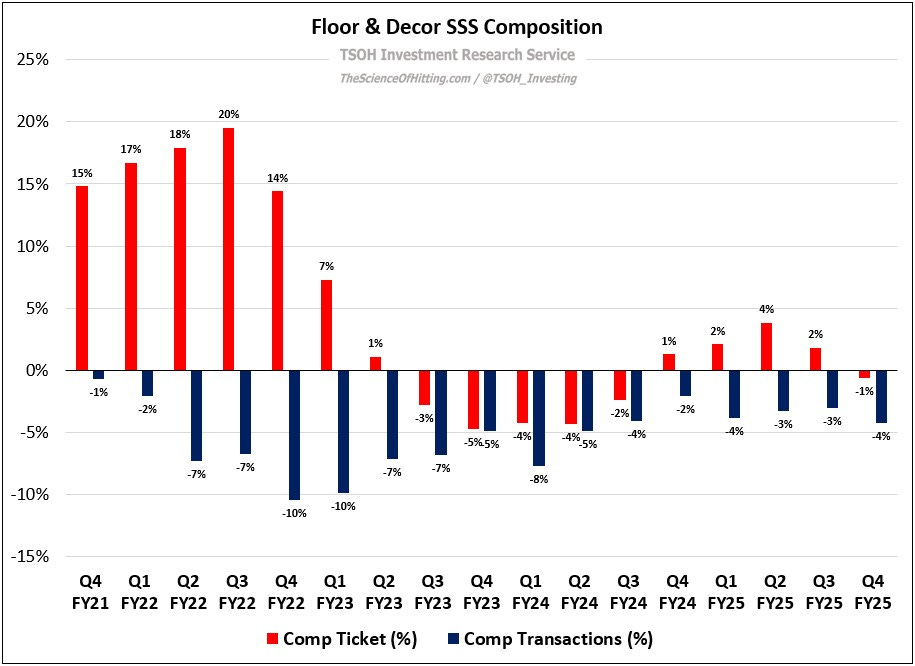

Floor & Decor’s Q4 FY25 results provided additional support for the cautious stance I’ve taken on the business, and particularly the stock, over the past three years. One metric that encapsulates this is comp transactions (traffic), which have contracted at FND in 17 consecutive quarters (-4% in Q4 FY25).

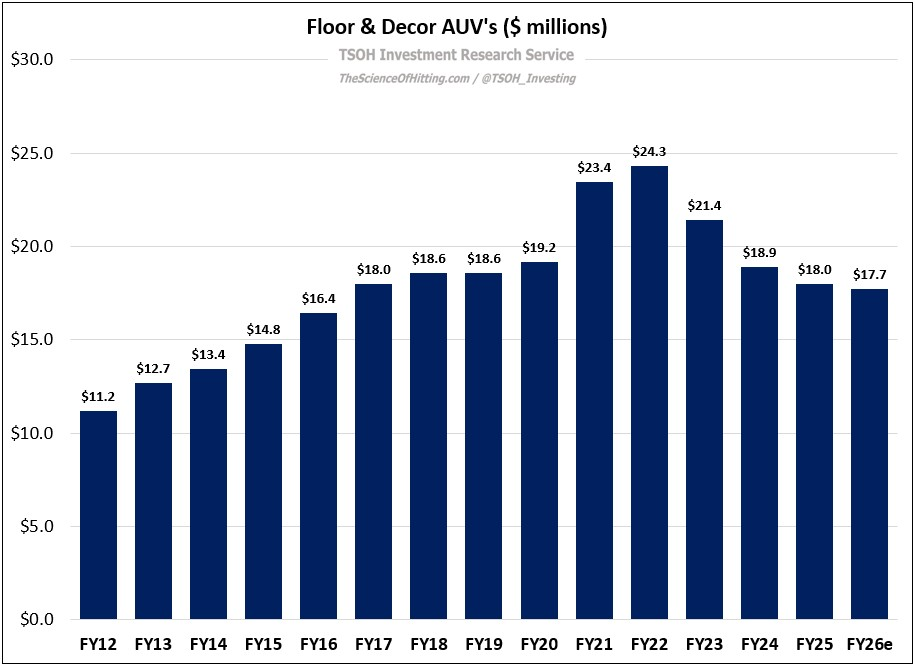

Management’s early FY26e guidance calls for continued comp pressure, with a low-single digit increase in average ticket offset by a low-to-mid single digit decline in comp transactions. As you can see below, guidance implies FY26e average unit volumes of ~$17.7 million – returning to levels first reached a decade ago, and down >25% from the peak levels reported back in FY22.