Fever-Tree: "Spreading Our Wings"

From “Fever-Tree: A Broader Opportunity” (April 2024):

“Despite success in premium carbonated mixers, my concern is that FT’s experience in the UK may point to a relatively limited opportunity in the core business… While it’s still early days, I think we’re seeing that the long-term opportunities for the Fever-Tree brand can extend beyond its original range.”

My high level takeaway from the 1H FY24 management presentation is that Fever-Tree is moving even more aggressively towards that broader strategic vision. Amidst ongoing pressure in UK Tonics, FT’s mix continues to shift to other products and regions. That could prove to be a fortuitous long-term development: I believe the company is positioned to be a long-term winner in certain categories, most notably cocktail mixers and premium sodas; if their aggressiveness in chasing these newer opportunities is accelerated as a result of maturation within UK Tonics, that could be a blessing in disguise.

That said, it presents a somewhat difficult financial profile in the interim, which has been the case for a few years and is still a consideration in FY24.

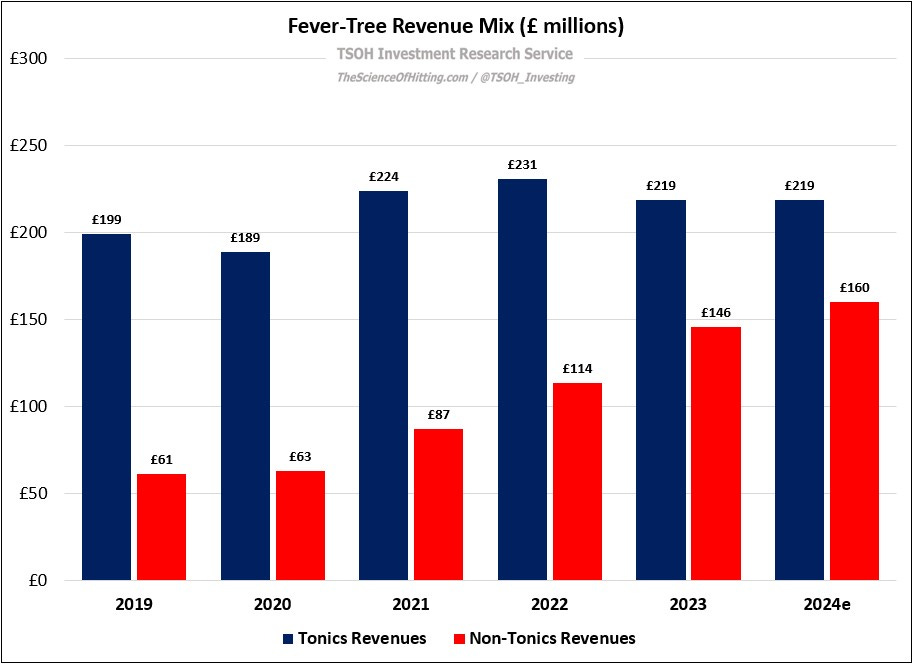

Based on disclosures in the 1H FY24 deck (slide five), we can guesstimate that Non-Tonics will reach ~£160 million in FY24e revenues, with a trailing five-year revenue CAGR of >20%. On the other hand, Tonics still account for the majority of the mix, with FY24e revenues of ~£220 million – and with a trailing five-year revenue CAGR of only ~2%. As I’ve discussed previously, I don’t think that this is (primarily) reflective of competitive considerations or other addressable / short-term pressures; put simply, there’s only so much growth ahead in Tonics. (It didn’t help that the beginning of this period was near the peak for UK gin – “more gin was sold during the three months of summer 2018 than in the summer months of 2014 and 2015 combined”).