Dollar Tree: Resilient Progress

From “Dollar Tree: The First Inning” (March 2025):

“On the checklist of items that were imperative to my Dollar Tree (DLTR) investment thesis, selling Family Dollar was at the top of the list… It’s a key reason why Dollar Tree quickly became a top holding [at that time, a ~15% weighting in the TSOH portfolio]; after a decade on the sidelines, I believe that Dollar Tree is a very compelling investment opportunity.”

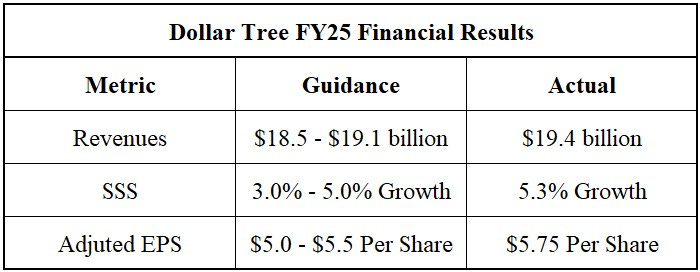

In March 2025, alongside the Q4 FY24 results, Dollar Tree management issued the following FY25 guidance: revenues of $18.5 - $19.1 billion (up ~7% YoY at the midpoint), comps growth of 3% - 5%, and adjusted EPS from continuing operations of $5.0 - $5.5 per share (up ~3% YoY at the midpoint).

Dollar Tree outperformed across the board in FY25: revenues increased by ~10% YoY to ~$19.4 billion, led by ~5.3% SSS growth, and adjusted EPS increased ~13% YoY to $5.75 per share, despite navigating unprecedented tariff pressures and the frictions / costs associated with “red dot” restickering.

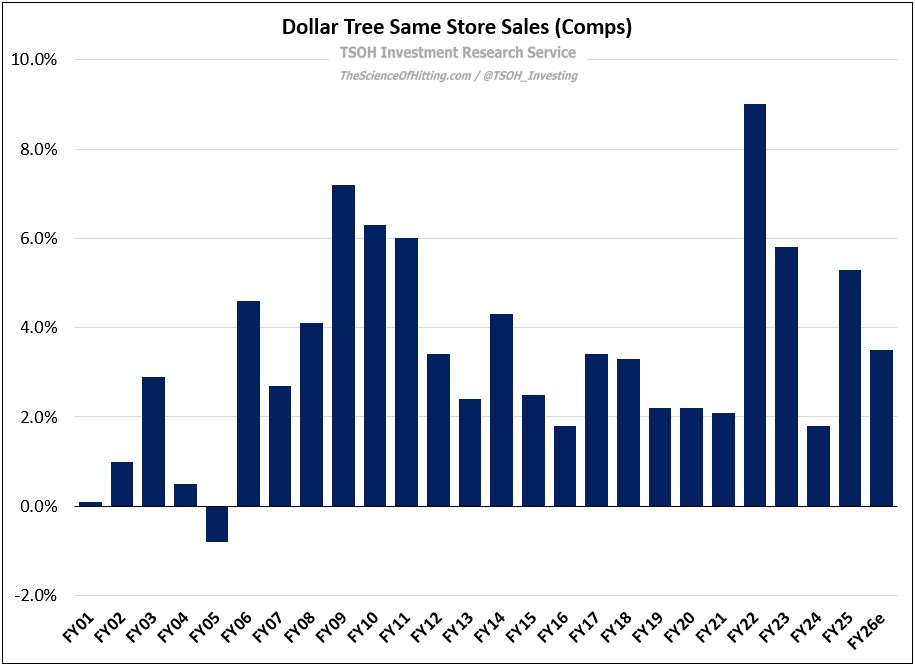

As we dig deeper, two things stand out in Dollar Tree’s Q4 FY25 comps.