Dollar Tree: "Value Creation Lever"?

In the December 2021 write-up “Breaking The Buck”, I reviewed Dollarama’s experience in Canada with its transition to a multi-price point value retail model as a case study for Dollar Tree’s recently announced strategic shift.

I concluded that post with the following:

“For now, I want to see the customer reaction to the early roll-out of the new pricing strategy; note that this change (and more notably DT+) also has potential long-term implications for Five Below, a company that I analyzed back in July [2021]. Over time, if it starts to become apparent that this strategic shift is bearing fruit, Dollarama’s experience over the past 10+ years suggests that it could have a long runway. Said differently, while the stock may appear optically expensive on FY22e EPS, that data point will be less relevant if we come to reasonably expect a significant ramp in earnings growth (from FY09 – FY21, Dollarama EBIT compounded at ~17% p.a.).”

It’s been nine months since Dollar Tree announced that tweak to its pricing, and I’d like to take the opportunity in today’s post to assess the early results, along with an update on the broader Dollar Tree story (most notably the ongoing Family Dollar turnaround efforts, which I spoke about in the June 2021 DLTR deep dive). As management noted last November, the first phase of the shift was a higher initial markup / price point at all Dollar Tree stores:

“This decision is permanent and is not a reaction to short-term or transitory market conditions. The $1.25 price point, which will apply to a majority of Dollar Tree’s assortment, will enhance the Company’s ability to materially expand its offerings, introduce new products and sizes, and provide families with more of their daily essentials.”

The other noteworthy part of the strategic shift was to introduce a multi-price strategy, called Dollar Tree Plus (DT+); this brought $3 and $5 SKU’s into the stores (accounting for ~10% of the selling space), with management setting an initial target of ~2,000 DT+ locations by yearend FY22, or ~25% of all Dollar Tree banner stores (they’ve already crossed that milestone, with the multi-price assortment available in 2,170 stores at the end of Q2).

Through the first six months of FY22, the impact of these changes in evident down the P&L; looking specifically at the Dollar Tree banner, 1H same store sales (SSS) increased by ~9%, with overall banner revenues climbing ~12% to $7.35 billion (DLTR banner unit count +2% YoY). The composition of this sales growth is worth thinking about. If we assume a ~25% lift in average selling prices versus the year ago period (our best guess for now), that would imply a low teens decline in unit volumes. In terms of price elasticities, it appears that Dollar Tree customers have largely accepted the $1.25 price point, which aligns with some of the survey findings that the company shared in November 2021: “91% of those surveyed indicated they would shop Dollar Tree with the same or increased frequency.” (It’s also worth noting that the 2H FY22 guide implies ~10% two-year stacked comps for the banner, a slight acceleration from the +7% two-year stack reported in Q2.)

As I discussed in “Breaking The Buck”, I think this positive result isn’t particularly surprising; it’s likely reflective of DLTR’s relatively unique merchandising and value proposition in certain product categories like party goods, arts and crafts, and greeting cards (in the Consumables category, I’d expect the price hikes will largely be reinvested to improve product quality, expand pack sizes, etc.). As a consumer, I do not get the sense that the higher price point in the unique product categories will cause customers to flee Dollar Tree; said differently, the products offered for $1.25 in arts & crafts, greeting cards, helium balloons, etc., are still a good value relative to the alternatives generally available in U.S. retail. (Anecdotally, I bought a birthday card earlier this week at the U.S. grocery store chain Publix for $3.79; that may help one to appreciate why the $0.25 price increase at Dollar Tree is effectively a non-issue in certain categories.)

This comment, from the Q2 call, speaks to the balanced performance across Dollar Tree’s product categories: “Consumables, which represented 47% of the Q2 mix, comped at 7.9%, while discretionary increased 6.7%. The last time the consumable comp exceeded discretionary was at the onset of the pandemic [Q1 2020]. This demonstrates the success we are seeing in key traffic-driving categories where our merchants have been active in enhancing value, such as carbonated beverage, snacks and cookies, and food. As a reminder, our reassortment in consumables has been more immediate than in discretionary given the purchasing cycle… Consumables momentum is a good indicator for the long-term health of the banner.”

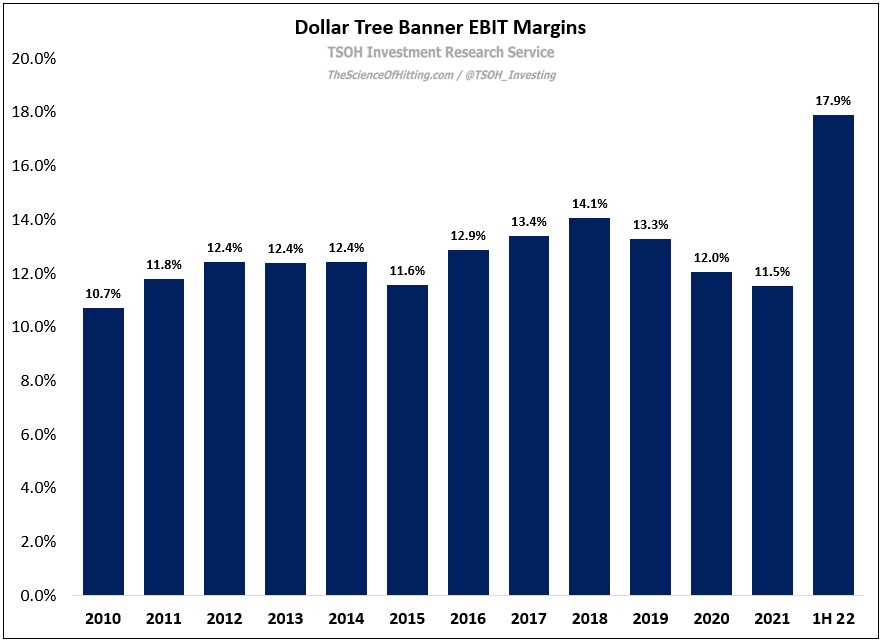

The biggest impact from this change is showing up on DLTR’s margins and profitability. In 1H FY22, the banner generated $2.87 billion in gross profits – up 32% YoY, with banner gross margins expanding 600 basis points (to 39.0%). Over the same period, banner operating income increased 80%, to $1.32 billion, with margins climbing 680 basis points (to 17.9%).