"A Structural Shift in Demand"

A look at Microsoft's 1H FY22 financial results

In November, I opened the Q1 Microsoft update with the following:

“In reviewing the quarterly results, I was reminded of something that comes to mind periodically: it’s much more enjoyable to review the performance of, and to be the long-term owner of, a company that is firing on all cylinders (and where the investment question inevitably comes down to the valuation) than it is to dig through the messiness of a business that consistently struggles to execute but which trades at a seemingly ‘cheap’ valuation. (Alas, whether the former offers the prospects of better returns is what truly matters.)”

On Tuesday, Microsoft reported results for Q2 FY22 – and with the proper long-term framing, I think its safe to say that the company continues to fire on all cylinders. But before focusing our attention on the results for the past 90 days, I wanted to share a high-level takeaway of how I think about Microsoft’s performance over the past few years: As I look across its various businesses – from Xbox / gaming and Azure to LinkedIn / advertising and Office (to name just a few) – what I see over and over again is how meaningful (organic and inorganic) investments, along with long-term strategic vision and effective execution, has led to sustained improvements in their competitive positions, revenue growth rates, and business values.

The combination of these factors - attractive end markets, strategic vision, an ability and willingness to invest for the long-term, and execution - is what has driven the company’s strong business performance over the past 5-10 years, and it’s what supports my belief that this will continue over the coming 10+ years. This, in my mind, is what truly matters for investors (and as a result, it’s where I focus my attention). Over the long run, whether Azure’s sequential growth rate decelerates or accelerates by a few hundred basis points in any given quarter due to short-term external pressures (not competitive factors or questions about the long-term TAM), a focal point for Wall Street analysts when the Q2 results were released, is just noise.

With that, let’s take a closer look at the Q2 and 1H FY22 results.

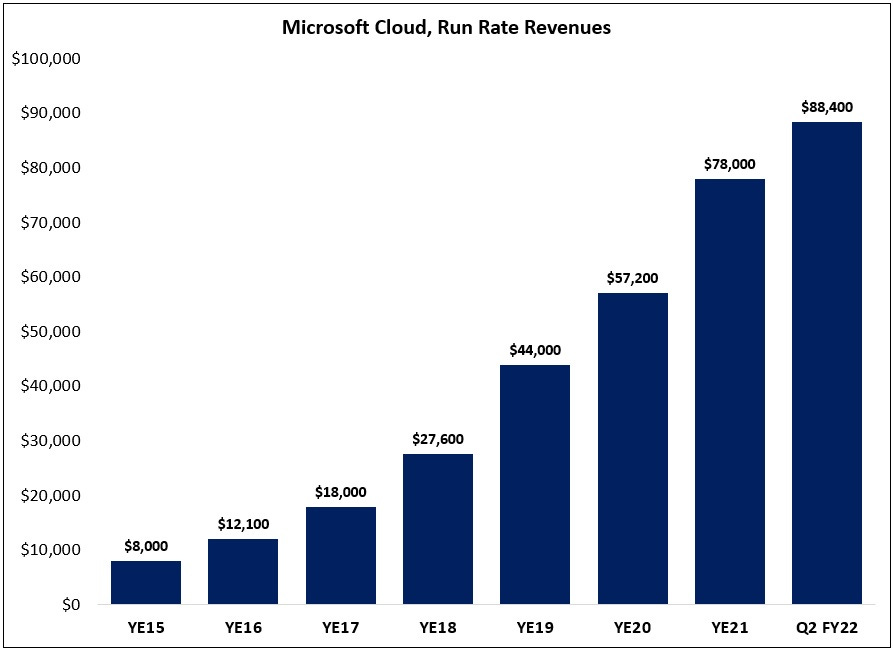

The Microsoft Cloud businesses reported 32% YoY growth in Q2, with run rate revenues climbing to $88.4 billion – more than 3x higher than the run rate at yearend FY18 and larger than Microsoft’s total revenues in FY14 ($86.8 billion). Needless to say, the “cloud first” world view that CEO Satya Nadella has preached for the past eight years has been transformative.