"Time Is Of The Essence"

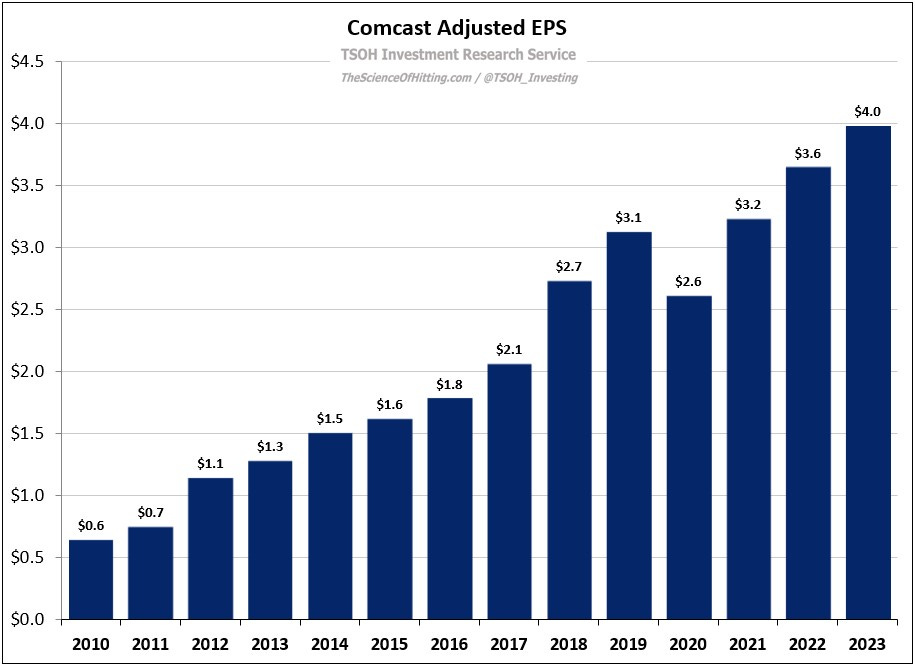

On Thursday, Comcast reported financial results for the final quarter of 2023. In light of current headwinds in connectivity and in the media business, the overall results were satisfactory, with adjusted EBITDA and adjusted EPS both reaching record highs (with the latter up 9% YoY to $4.0 per share).

On the company’s quarterly call, following introductory remarks from other members of the management team, CEO Brian Roberts said the following:

“We have a unique company that is incredibly well positioned. We always try to think about and invest for the long-term... In 2023 alone, we returned $16 billion to shareholders. It's also the 16th straight year that we’ve raised our dividend. That's consistency… We’re making the right adjustments to our businesses to position us to win, grow, and continue to return capital to our shareholders. And while there may be speculation of what we could do next, I'd like you to hear it directly from me: I love the company we have. The bar continues to be even higher for us to do anything other than the plan you heard today.”

While Comcast’s broadband business continues to face volume pressures, with management’s commentary suggesting that they do not foresee material improvements in 2024, they’ve also done a good job of holding their position in the face of a period of heightened competitive intensity. (As a reminder, the Connectivity & Platforms segment accounts for roughly 80% of Comcast’s EBITDA.) If one has confidence in Comcast’s ability to weather the current pressures in broadband, that presents an interesting setup for shareholders.

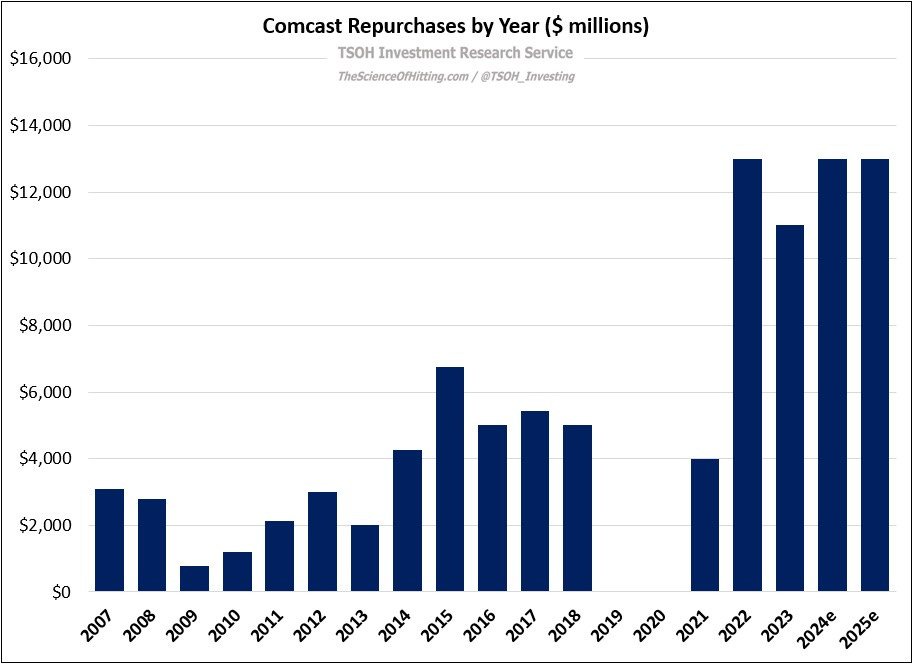

A big reason why is the pace of capital returns.

As you can see below, Comcast repurchased ~$45 billion of its common stock over the 15-year period from 2007 to 2021. By comparison, I think the company is likely to repurchase ~$50 billion of stock over the four-year period from 2022 – 2025, inclusive of more than $25 billion over the next 24 months. (To put that figure in context, Comcast’s current market cap is ~$185 billion.)

That thesis rests on three key assumptions: (1) the stability / growth of the Connectivity & Platforms segment; (2) the stability / growth of the Content & Experiences segment; and (3) capital returns, i.e. resisting transformative M&A. In today’s post, I’ll provide an update on each of the three buckets.