Roblox: Reality Check

Note: Click here to access all prior Roblox (RBLX) research

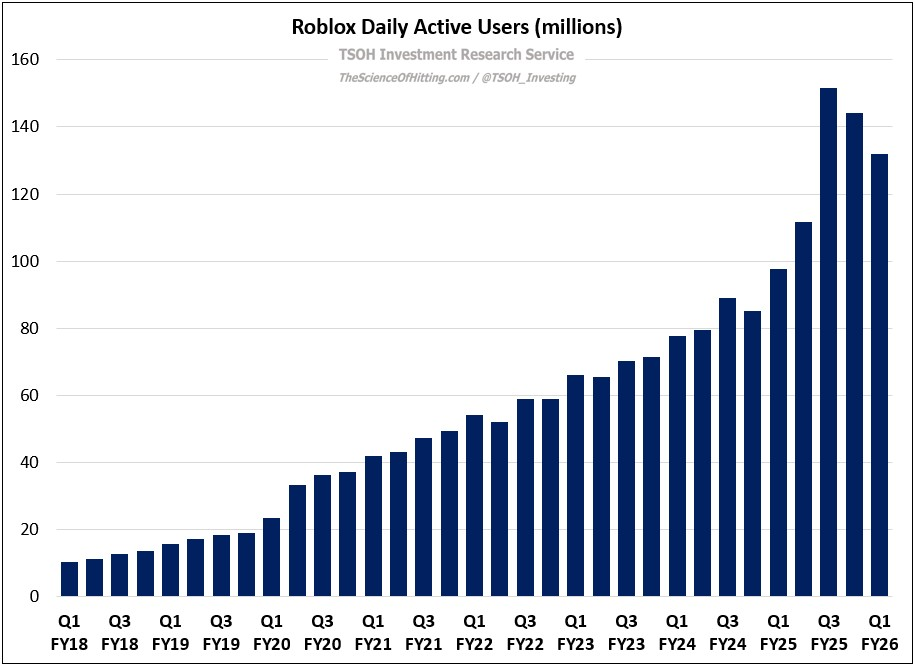

In October 2025, following Roblox’s Q3 FY25 results, one prominent Wall Street analyst published a note that included the following glowing comment: “Roblox printed arguably its strongest quarter ever.” While it was hard to quibble with that framing given the daily active user (DAU), engagement, and booking trends Roblox reported at the time, it struck me as reason to be cautious on the stock, at least in the short-term. In recent years, Roblox has seen sizable swings on user / engagement growth, followed by a muted response from management on its pace of expense growth; said differently, the stellar 2H 2025 growth would likely give way to an eventual period of relatively lackluster DAU / bookings growth, with outsized pressure on profitability and FCF generation. When that day arrived, near term bookings and margin estimates would be cut, and short-term optimism would fade.

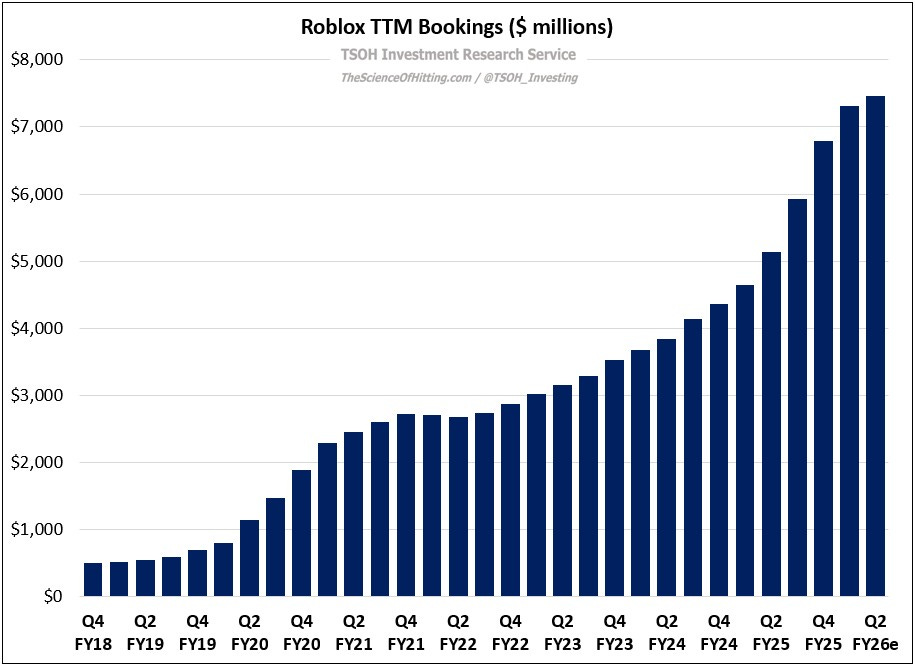

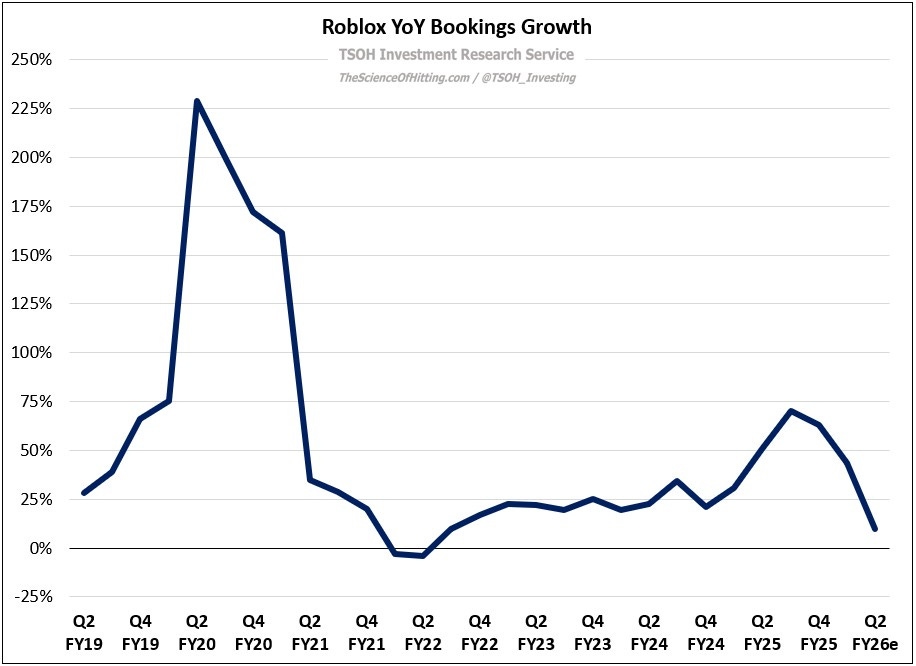

Jumping to the present, we can see that this is what has happened: when Roblox reported Q1 FY26 results last week, management reduced FY26e bookings growth from +24% to +10% (midpoint), but with little indication this will result in any material change to FY26e spending. As a result, they now expect FY26e FCF of ~$1.2 billion, down ~30% from earlier expectations.

The stock, which eclipsed $140 per share in September 2025 (seven months ago), has since fallen ~70% to ~$45 per share. As a result, the stock trades about 40% lower than where it did after the March 2021 direct listing – and that’s over a period where TTM bookings more than tripled to ~$7.5 billion.

I think the long-term Roblox thesis comes down to two key issues: