"I've Seen This Movie Before"

In hindsight, the idea of bucketing companies into COVID “winners” and “losers” looks overly simplistic and short-sighted. For most of the businesses that I follow, the tailwind or headwind experienced in the first 12-18 months after the onset of the pandemic has become a mixed bag (at best); and in its wake, we’re left with difficult questions about what a “normal” future looks like. The upside? With this recent bout of difficulty in the stock market, I believe that unpredictable short-term business volatility is presenting some interesting opportunities for investors who can sift through the rubble and find companies that are well positioned to generate outsized long-term returns.

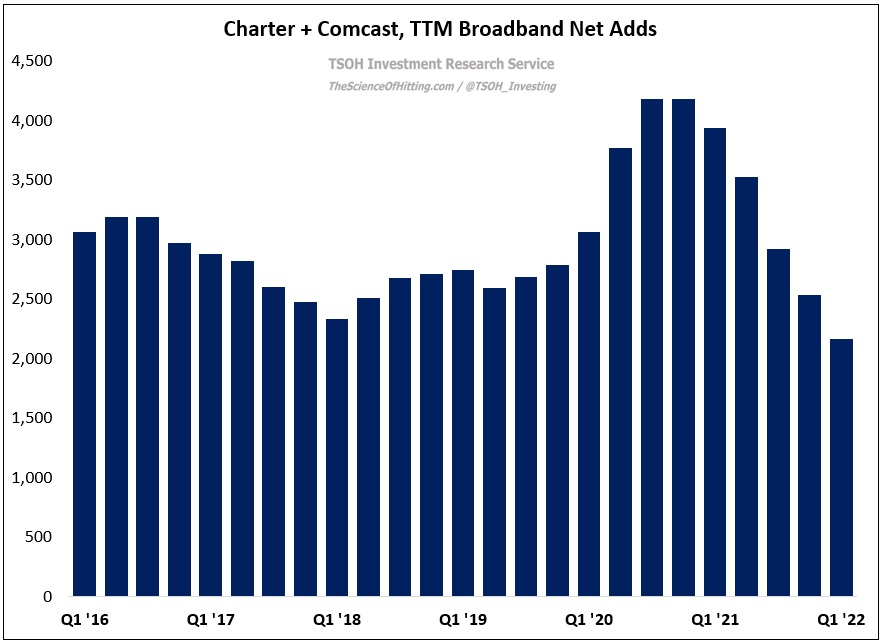

One example, in my opinion, is Cable. For Comcast and Charter, the pandemic provided a sizable tailwind out of the gates: for example, in 2020, they collectively added 4.186 million net broadband customers – 50% higher than the 2.786 million net broadband customers collectively added in 2019.

The problem is that the pace of net adds has decelerated meaningfully over the past year. At Comcast, Q1 FY22 sequential broadband net adds were +262k, compared to a trailing five-year Q1 average of +419k; at Charter, those numbers were +185k and +437k, respectively. (And even those results are inflated: as Comcast noted, net adds included ~80k customers who received free service during the pandemic and paid for the first time in Q1.)

The market’s concern, in my opinion, is the nature of this deceleration; is it indicative of the pandemic pull forward / other external factors (meaning a return to the mid-single digit net broadband growth that Charter and Comcast consistently reported in the years before the pandemic), or is it attributable to other factors - most notably, heightened competition - that fundamentally change the long-term prospects for these companies?