Flutter: Parlaying DFS To OSB

In November 2016, after four years of fighting for the pole position in the U.S. daily fantasy sports (DFS) market, DraftKings and FanDuel announced their intention to merge. The impetus for the deal was an extended period of significant promotional / advertising spend as the companies fought each other for market share, along with an uncertain regulatory landscape that threatened the viability of their end market (“several state AG’s said the sites violated state gambling laws”). But just eight months later, in July 2017, the proposed marriage was called off following an antitrust lawsuit from the FTC.

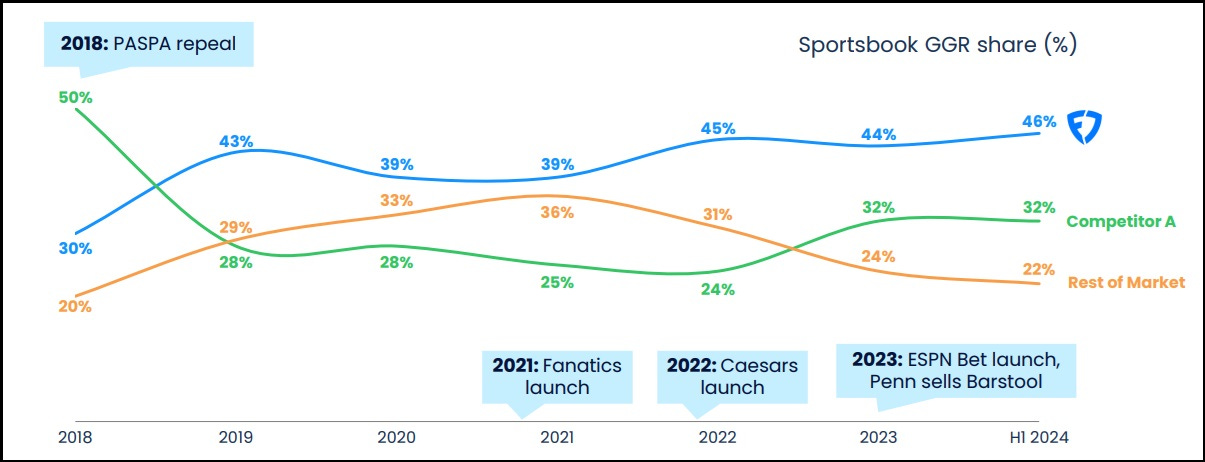

The next big industry development came in May 2018, when the U.S. Supreme Court ruled that the Professional and Amateur Sports Protection Act of 1992 (PASPA) was unconstitutional; as a result, the door was opened for legalized sports betting in the U.S. (outside of Nevada). Three months later, in August, DraftKings first online sportsbook (OSB) opened in New Jersey.

Over the next five years, a long list of competitors threw huge sums of money at customer acquisition, with the goal of gaining share in the nascent OSB / iGaming market. For example, when Caesars launched in New York in early 2022, they offered new customers a $300 free bet, along with a 100% deposit match up to $3,000. (Now, you are lucky if you can find a $1,000 match.)

Given that May 2024 was the six year anniversary of PAPSA’s end, it is interesting to note that the two big DFS players have managed to sustain a dominant market lead: as shown below, Flutter (FanDuel) and DraftKings accounted for 46% and 32%, respectively, of the U.S. OSB market as of 1H FY24, with all other competitors ceding roughly ten points of share in the past two years. As I will discuss in today’s write-up, I believe this outcome reflects certain sustainable competitive advantages that the other OSB’s have not, and will not, overcome. (As a Disney shareholder, I’d be remiss if I didn’t mention how poorly they have played their hand with ESPN; they were late / noncommittal in OSB, and then failed to strike a deal at an opportune time.)