Ally Financial: In Gear

From “The Importance Of Focus” (April 2025):

“Given some of the decisions made in the past year, along with an improving trajectory in credit, I am optimistic about what lies ahead for Ally. As it relates to the current attractiveness of the stock, note that CFO Russ Hutchinson has bought ~$1 million on the open market in recent months [he added another ~$500k in January 2026]… If the deposit gathering franchise meets my long-term expectations, along with sound credit underwriting and meaningful capital returns (particularly if the shares trade, on average, at less than 10x forward earnings), I think the stock will generate attractive returns over time.”

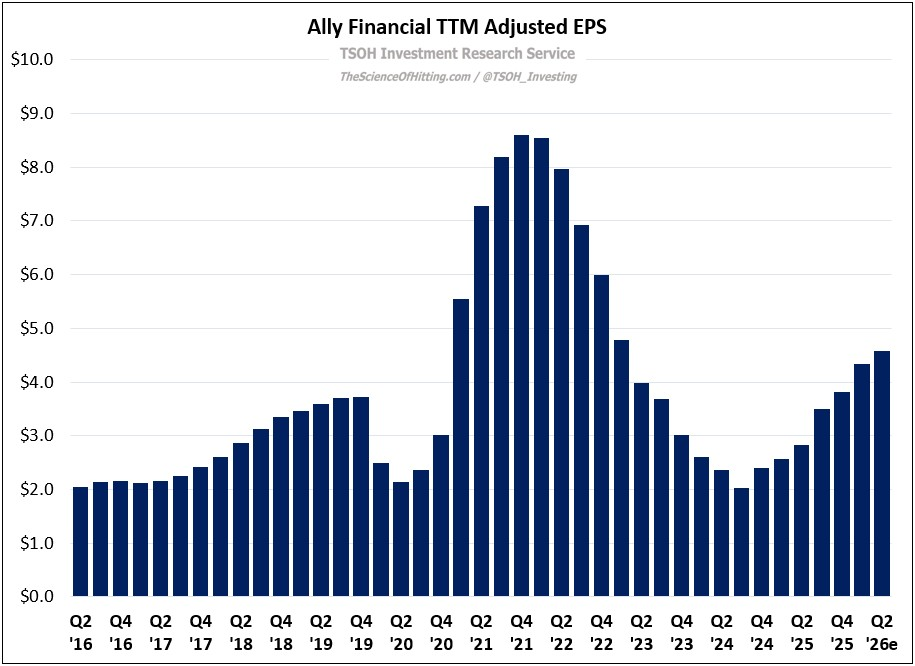

ALLY has seen a solid resurgence of late: the stock is up ~40% over the past year and has doubled since YE 2022 (TSR). This recent price increase has still lagged its strong earnings recovery, with Q1 FY26 TTM adjusted EPS up ~70% to ~$4.3 per share. (On an annual basis, I estimate FY26e EPS at ~$5.3 per share - up ~125% from the FY24 EPS trough of ~$2.4 per share.)

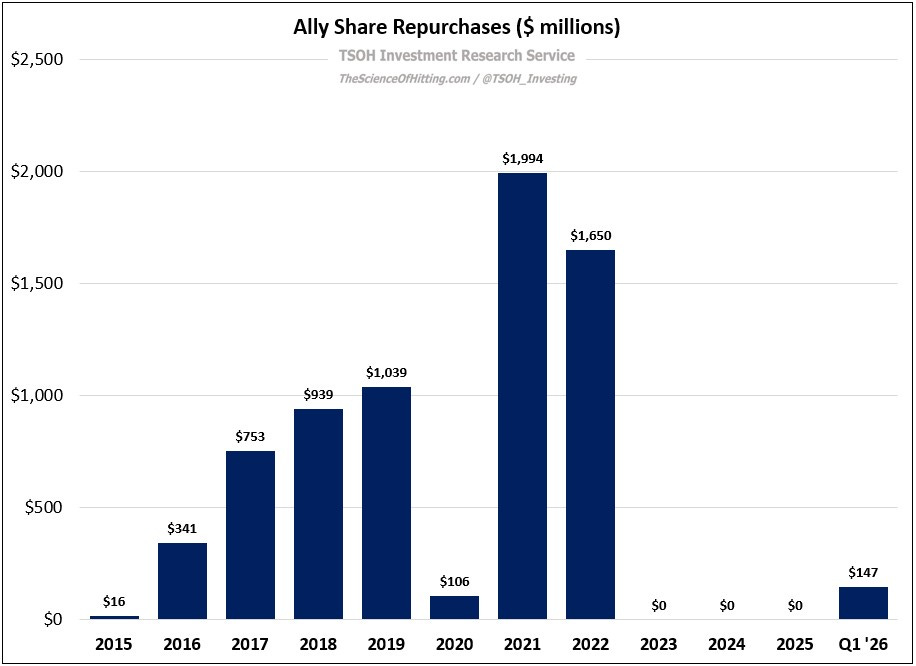

Said differently, despite a nice run to ~$44 per share, it still trades at 8x – 9x forward on FY26e EPS - and I think an EPS CAGR of ~15% is likely over the ensuing two years, to >$7 per share in FY28e. On the EPS drivers, note that Ally bought back ~$150 million of stock during Q1 FY26, the first time they’ve repurchased shares in more than three years; this will likely be a meaningful tailwind to the TSR algorithm through FY28e. (In addition, revised capital requirement proposals could lead to a ~100 basis point lift in Ally’s CET1 relative to the 2023 proposal, providing room for balance sheet flexibility.)